The root cause isn’t poor vendor selection or underinvestment—it’s an unresolved architectural question: Which system governs behavior across cash management, workflow, compliance, and reporting? When this question remains unanswered, responsibility diffuses across platforms, manual processes proliferate, and technical debt accumulates.

As advisory assets have outpaced trust assets, the assumption that the trust accounting systems can serve as the universal operating pillar has become misaligned with how wealth businesses function. Banks have responded by layering modern tools onto trust-centric cores. While these additions improve visibility, they do not resolve conflicts around cash management, workflow ownership, and system authority. The result is platform friction that surfaces as manual workarounds, rising cost to serve, and degraded advisor and client experience.

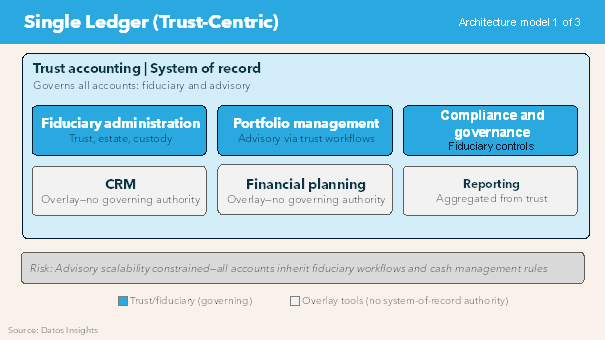

This brief examines three dominant architecture models: traditional trust accounting platforms as single-ledger systems, dual-ledger architectures with orchestration, and advisory-led hybrid stacks. Each performs durably when aligned with institutional identity. Each fails predictably when it is not. The analysis provides a framework for aligning architecture with growth strategy and helps executive teams recognize that the most consequential technology decision is not which platform to buy, but where advisory resides within the operating architecture.

About the Author