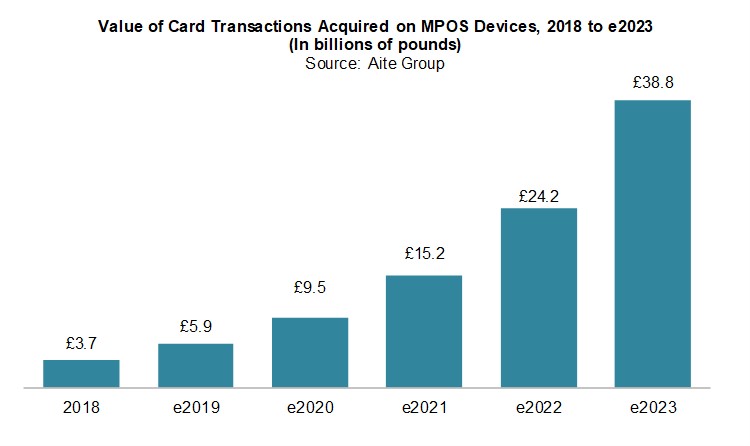

London, 18 July 2019 – The U.K. has seen strong adoption of mobile point of sale, a technology that was introduced about a decade ago as a card acceptance solution for small businesses—a niche segment that was not yet served by traditional acquirers. But driven by merchant demand for mobility, customer service, and integration of payments with electronic POS applications, mPOS technology is increasingly deployed by larger businesses. Can specialized mPOS providers compete successfully with mainstream acquirers that have come to the market with their own mPOS solutions?

This Aite Group report provides an in-depth view of the mPOS market in the U.K. It analyzes small and midsize merchants’ need for payment acceptance solutions, sizes the mPOS market as a segment of the overall U.K. POS payments market, and outlines the competitive landscape of mPOS solutions and their distribution channels. It is based on Aite Group’s late 2018 and early 2019 interviews of 16 executives from leading merchant acquirers, mPOS providers, card schemes, distributors/resellers, and technology firms active in the U.K. market.

This 23-page Impact Report contains 12 figures and one table. Clients of Aite Group’s Retail Banking & Payments service can download this report, the corresponding charts, and the Executive Impact Deck.

This report mentions Aevi, Apple, Barclaycard, British Airways, cab:app, DHL, Domino’s, Elavon, FirstData, Handpoint, Kounta, Ingenico, iZettle, Lightspeed, Lloyds Bank Cardnet, MyPINPad, NMI, O2 Arena, Paymentsense, Payworks, PayPal, Poynt, Spire, Square, SumUp, Ted Baker, Vend, Verifone, and Worldpay.

About the Author