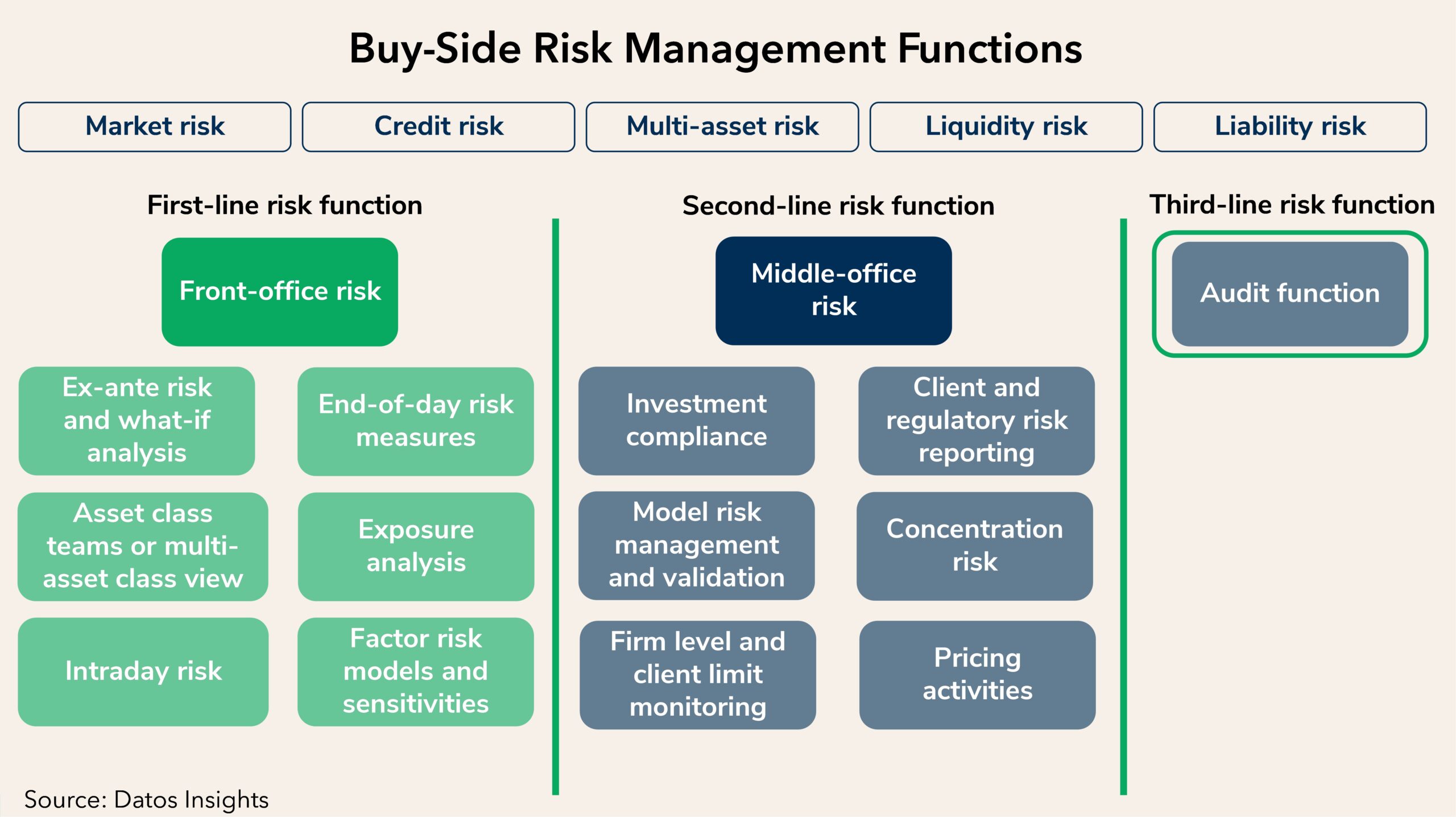

All investment managers (IMs) essentially have one goal: to fulfill their investment revenue charter and achieve revenue mandates within risk tolerances. The optimization of the risk/return profile is the lifeblood of portfolio management. Within the full investment life cycle are the first line of risk defense (front office: investment), second line (middle office: performance attribution), and third line (back office: regulatory). Financial risk management within IMs concentrates on the risk-return balance across investment management; risk and return are inextricably connected.

This first report in a series of two focuses on the front-office risk, concentrating on the components of risk-return development and management, and reviews the vendor landscape. Datos Insights engaged directly with the vendors involved with the investment managers’ (IMs) front-office risk offerings between January and April 2024 to get both insights and direct briefings of the capabilities presented in each of the vendor profiles, along with previous Data Insights’ research. This report profiles Bloomberg, FactSet, Finastra, FIS, Moody’s, MSCI, Numerix, Quantifi, S&P, SimCorp (Qontigo), State Street, and SS&C.

Clients of Datos Insights’ Capital Markets service can download this report.

This report mentions Bloomberg, FactSet, Finastra, FIS, Moody’s, MSCI, Numerix, Quantifi, S&P, SimCorp (Qontigo), State Street, and SS&C.

About the Author