Datos Insights held its 2023 Wealth Management and Capital Markets Forum on Tuesday, October 3, in New York City. The Datos Insights team was joined by 160 attendees, including senior representatives from nearly 80 different financial institutions participating in three plenary sessions and five wealth management track sessions, covering some of the topics our clients have identified as being most impactful over the course of 2023.

In this post, I’ll look to cover some of the key learnings that our team and I took away from the panelists’ conversations, focusing on a topic that permeated all of our discussions: personalization. (Discussions of artificial intelligence also threaded their way through virtually every panel, which I think is something that deserves a post of its own.)

Personalization: It’s Not Just for the Ultra-High Net Worth Anymore

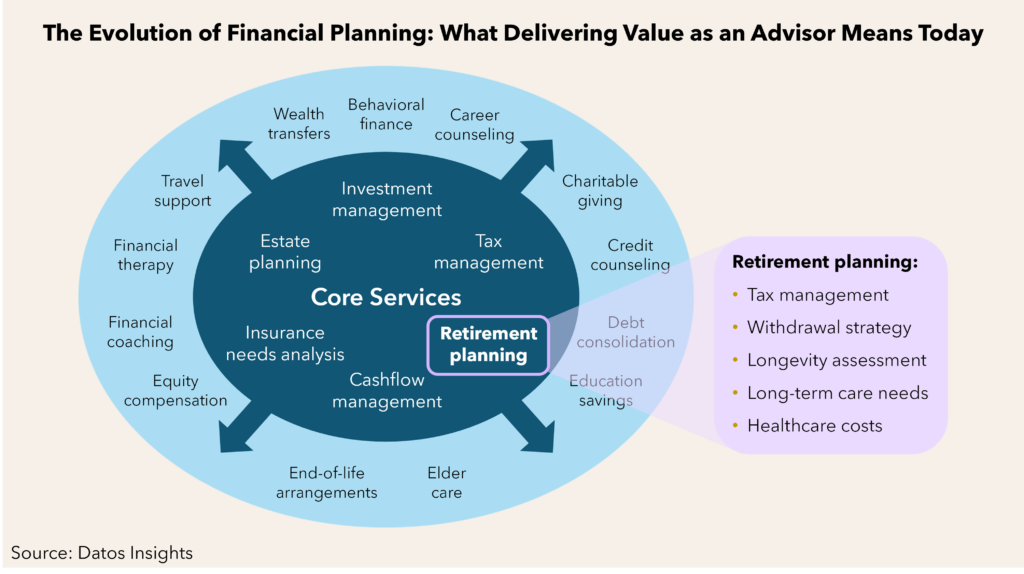

Personalization found its way into almost all of the Wealth Management breakout discussions, beginning with Lisa Asher’s panel Can Today’s Financial Planning Deliver on the Promise of Financial Wellness. The first point that struck me is that despite investors’ top concerns being around inflation, healthcare, and social security, many are continuing to increase their general spending behaviors. This increase in spending and a wave of “unretirement” by people who left the workforce during the pandemic have created new challenges for advisors around helping clients prepare for their actual retirements, including social security planning, helping with budgeting exercises and placing guardrails around excessive spending behaviors, as Figure 1 illustrates.

The other topic that struck me from this conversation is how big a shift in thinking and behavior is required from advisors and clients as planning for longevity becomes a critical factor in the overall retirement dialogue. The implications around healthcare are particularly striking—the concerns that terms like financial wellness can actually imply value judgments around a given client’s lifestyle, for instance—and the difficulty on both sides of having highly personal conversations that might historically have seemed more in keeping with a medical setting but have become critical for advisors to account for in order to deliver successful retirement outcomes that align with very specific healthcare requirements and longevity projects for individual clients.

Two panels that focused on the evolution of advisor technology platforms highlighted how the evolution of these tools is allowing advisors to drive personalization of service from efficiency, client access, and service model perspectives. In my panel, CRM: How to Attain Agility and Efficiency in the Client Journey, the discussion took us in the direction of how even the most core of core technology platforms—the advisor’s workflow-enabled CRM hub—can better facilitate the personalization of the client experience by surfacing key information, prioritizing it for an advisor to action and even wrapping that process around client service models.

In Wally Okby’s Digitizing the Customer Reporting Experience: Innovate or Be Left Behind, this concept was taken even further. Panelists discussed how advisors report that portals delivering relevant content and performance reporting to end clients create a much stronger experience for their clients and ease advisors’ pure servicing burdens. There is a competitive advantage for firms that deploy portals that update intraday, provide real-time views into transactions, holdings, and performance and can be accessed from any device. Much of that advantage is coming from the enhanced customer experience. Finally, the panelists see a proliferation of new features and functionality, such as customizable and interactive outputs, integration of wealth planning to mobile devices and tablets, and sustainable investment impact reporting. These features present unique opportunities for firms to build loyalty and brand recognition and provide clients with more consistent experiences.

Personalization is more than just planning or touches or investment product related, as David Himmel demonstrated with his panel on Building Bridges: Converging Channels to Acquire and Retain Clients. The panelists zeroed in on how marketplace offerings allow advisors to assemble more holistic product sets. These offerings incorporate financial products beyond investments that clients don’t always initially associate with a financial advisor, such as personal loans, mortgages, securities-based lending, cards, deposit accounts, and even risk products (e.g., automobile insurance), though all of them are relevant when providing holistic advice. The panelists particularly called out the evolution of APIs as having made these types of financial solutions so much more accessible for advisors and their clients, particularly as workflows around things like underwriting criteria can be incorporated into the API and allow decisioning to happen in near real time.

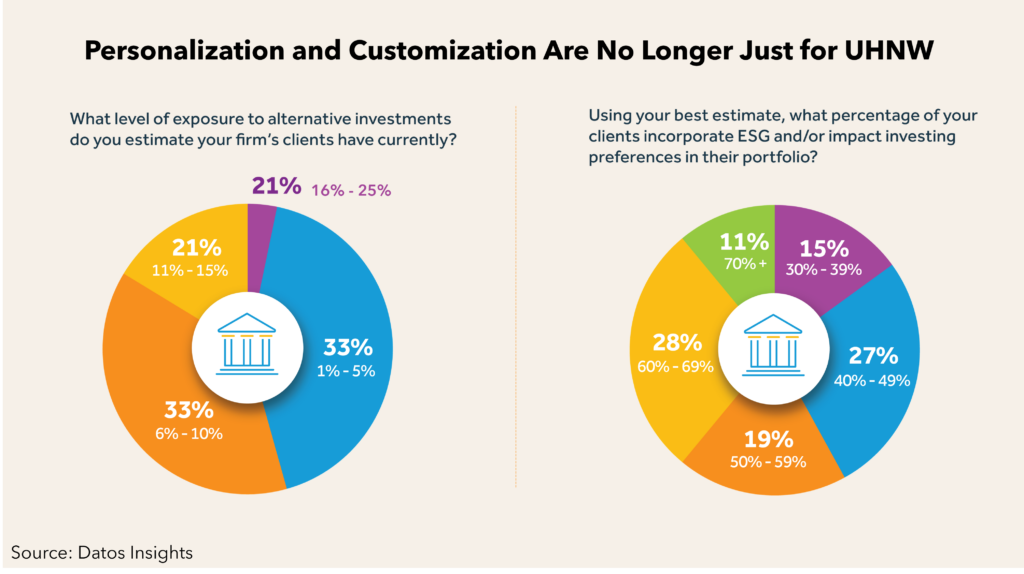

Finally, in my panel focusing specifically on the topic, Mass Personalization/Customization at Scale: Responding to the Voice of the Customer, we learned that personalization of investment product selection—in particular—is no longer the exclusive purview of the ultra-wealthy as also evidenced by the recent Datos Insights Flagship survey data related to alternatives and environmental, social, and corporate governance.

The key lesson from this panel is that technology has enabled the democratization of personalization when it comes to investment. Institution-quality models are available from core custody platforms as well as turnkey asset management programs that retain the flexibility for advisors to modify to meet the specific personal needs of their clients. Direct indexing and the ability to trade fractional shares have given end clients greater access to direct ownership of individual equity through models at a much lower cost of entry. Tax-aware/tax-sensitive management was probably the number one personalization factor that was raised by all of the panelists. Of course, it was also pointed out that in order to achieve the optimal impacts of mass personalization, you must first put your data house in order!

Many other topics were addressed in the course of a highly engaging day in New York City. In hindsight, it feels like the revolution of personalization across the advisor-client relationship—from the data that underlies it and the way it’s served up and prioritized to the solutions that are becoming available and how an advisor can deploy them to optimal effectiveness for their clients was a key theme, and one that will have a strong carryover into key industry trends in 2024.

If you’d like to dive deeper into how personalization is impacting the advisor/client relationship, see Navigating Pathways to Holistic Wealth Management by my colleague Wally Okby. For more information around Direct Indexing as a tool for mass personalization, see Datos Insights’ report The Direct Indexing Opportunity: Poised for Growth.