Boston, December 10, 2020 – The digital acceleration in retail banking has given rise to a proliferation of digital-only banks. These neobanks interact with their customers exclusively through digital channels and have differentiated their offering from that of traditional banking by focusing on the customer experience. But can neobanks independently scale, build a profitable banking business, and remain independent, or will they find themselves usurped or absorbed by incumbents?

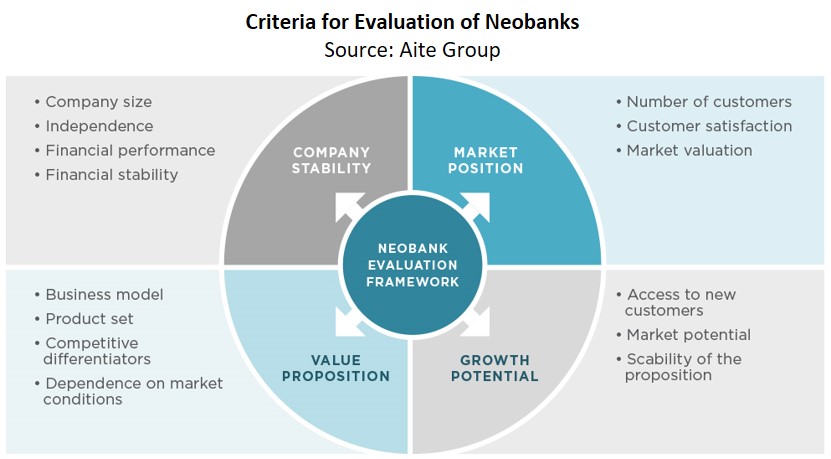

This report gives an overview of the current neobank landscape. Based on Aite Group’s 2020 interviews with executives from 21 leading organizations, including neobanks, traditional banks, and technology providers in the banking industry, it examines neobanks’ value proposition and defines various categories of neobanks, the business models and strategies they deploy, and the criteria for success.

This 34-page Impact Report contains 12 figures and five tables. Clients of Aite Group’s Retail Banking & Payments service can download this report, the corresponding charts, and the Executive Impact Deck.

This report mentions 3Cinteractive, Abe AI, ABN Amro, Accenture, Active.Ai, Acuant, Acxiom, Albert, Allied Payment, Ant Financial, ARIADNEXT, Asto, Atom Bank, Avaamo, Backbase, Banco del Sol, Bank Mobile, BankSight, Barclays, Beyond the Arc, B-North, BNP Paribas, Bold360, BOND.AI, Bottomline Technologies, Brighterion, bunq, Capco, Chime, Clinc, Conversation.one, CU Direct, CustomerMatrix, Customers Bank, Datameer, Deloitte, Deluxe Marketing Solutions, DemystData, digibank, Digital Onboarding, DocuSign, dunnhumby, EdgeVerve, Eloqua, Epsilon, Equifax, eSignLive, Experian, EY, Feedzai, Fenergo, FICO, Fidor Bank, Finastra, Fincog, Finn AI, FIS, Fiserv, Five Degrees, Gravity Online Bank, Gro Solutions (Q2), Halifax, Harland Clarke, Hay bank, Hello bank, HSBC, Humley, IBM, ID Analytics, IDology, imaginBank, Intellect Design Arena, IPsoft, Jack Henry & Associates, Jumio, KakaoBank, KakaoTalk, Kasisto, Knab, Kofax, Kore.ai, KPMG, La Caixa, LexisNexis Risk Solutions, Lexmark, Lloyds Bank, Lunar Way, Mambu, Marcus by Goldman Sachs, Marketo, Marquis Data, MeridianLink, Merkle, Mettle, Mitek, Monese, Monzo, Mybank, N26, Nationwide Building Society, NatWest, nCino, NCR, New10, Newgen, Next IT, NGDATA, Nielsen, Nimble, NinthDecimal, Nordea, Novantas, Nuance Communications, Nubank, OakNorth, Ondot Systems, OneSpan, Onfido, Oracle, P.F.C., Paycasso, Payjo, Paytm Payments Bank, Pegasystems, Personetics Technologies, PwC, Qapital, Radius, Recognise Bank, Revolut, Revverbank, RILA GLOBAL, Royal Bank of Scotland, Santander, SAS Institute, Segmint, ServiceNow, Signicat, Simple, Simplii Financial, Smart Engine, SoFi, Space Bank, Starling Bank, Syncrement, TalkBank, Tandem Bank, Tata Consultancy Services, Temenos Group SA, Tencent, Terafina, Tink, Tinkoff Bank, TransUnion, Treasury Intelligence Solutions (TIS), TymeBank, Vantedge, Varo Money, Virgin Money Australia, Wally, WeBank, Zenmonics, Zoot Enterprises, and Zylotech.

About the Author

Other Authors