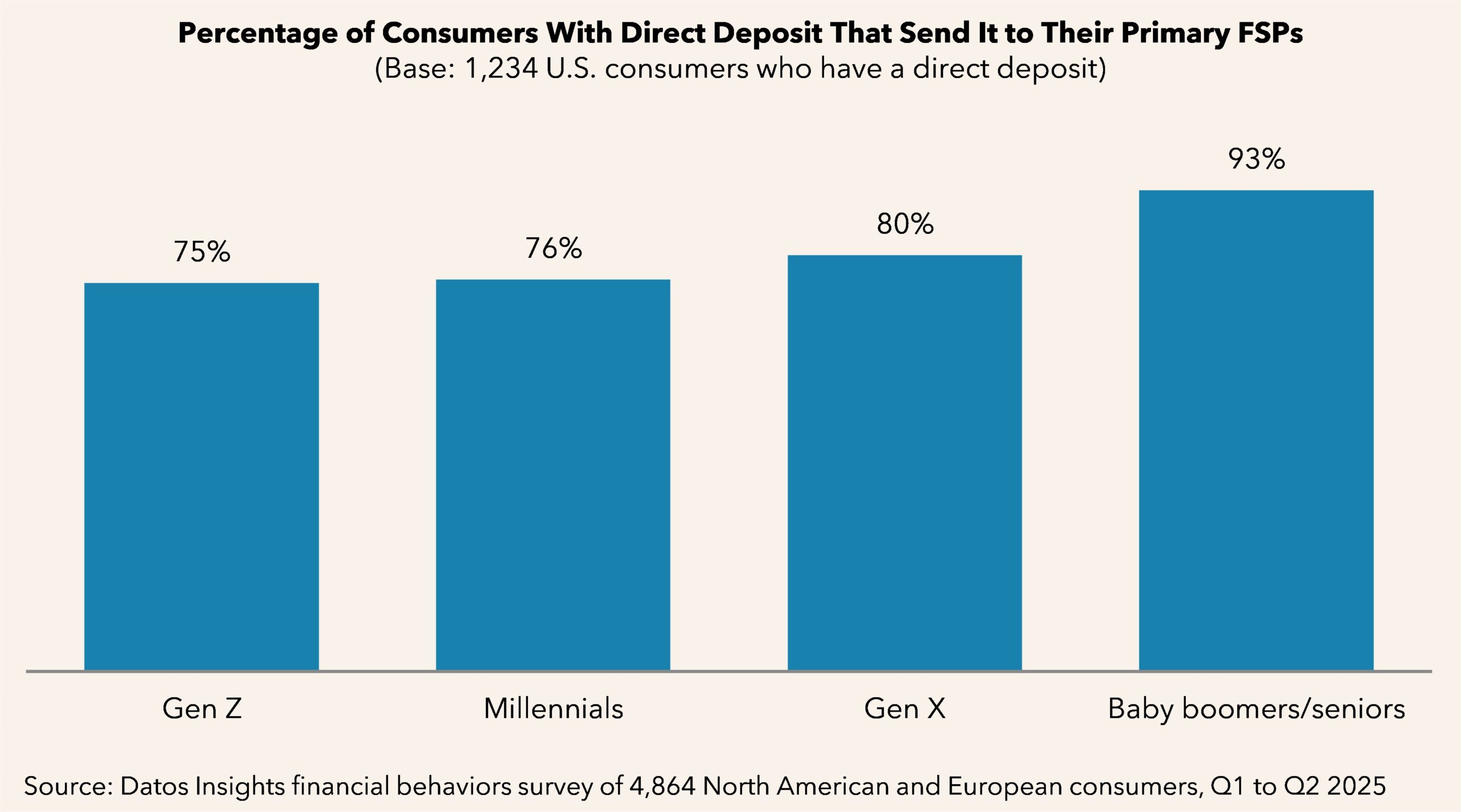

Despite over 9,000 banks and credit unions available to consumers, the “Big Four” banks capture 41% of primary banking relationships, the top three alone holding 10% or 15% market share. While primary relationships remain relatively stable with consumers typically maintaining their chosen institution for years, Datos Insights research reveals trends that suggest traditional anchors of these relationships are weakening. Services such as bill payment services and direct deposit are slipping. Only 16% of customers use bill payment services with their primary FSPs and direct deposit is being lost to fintechs that offer flexible payroll options such as earned wage access and credit-building tools.

This report examines the evolving nature of primary banking relationships in the United States amid increasing financial flexibility and growing competition from digital challengers. The analysis is based on three comprehensive consumer studies: one among 1,500 U.S. consumers in Q1 2025, one among 2,500 U.S. consumers in Q1 2024, and another among 2,006 U.S. consumers in Q3 and Q4 2022.

Clients of Datos Insights’ Retail Banking & Payments service can download this report.

This report mentions Bank of America, Chime, Citibank, JP Morgan Chase, and Wells Fargo.

About the Author