September 21, 2022 – Competition for clients and producers, including agents, is high. Insurers continue to look for ways to improve the customer experience while creating competitive advantages through enhancements to products and services. Video collaboration with policyholders on claims is one avenue insurers are exploring.

This report provides an overview of personal lines insurer business and technology issues, data about the marketplace, and more than 20 examples of recent insurer technology investments. It is based on the expertise of Aite-Novarica Group’s staff, conversations with Aite-Novarica Group clients and Insurance Technology Research Council members, and a review of secondary published sources.

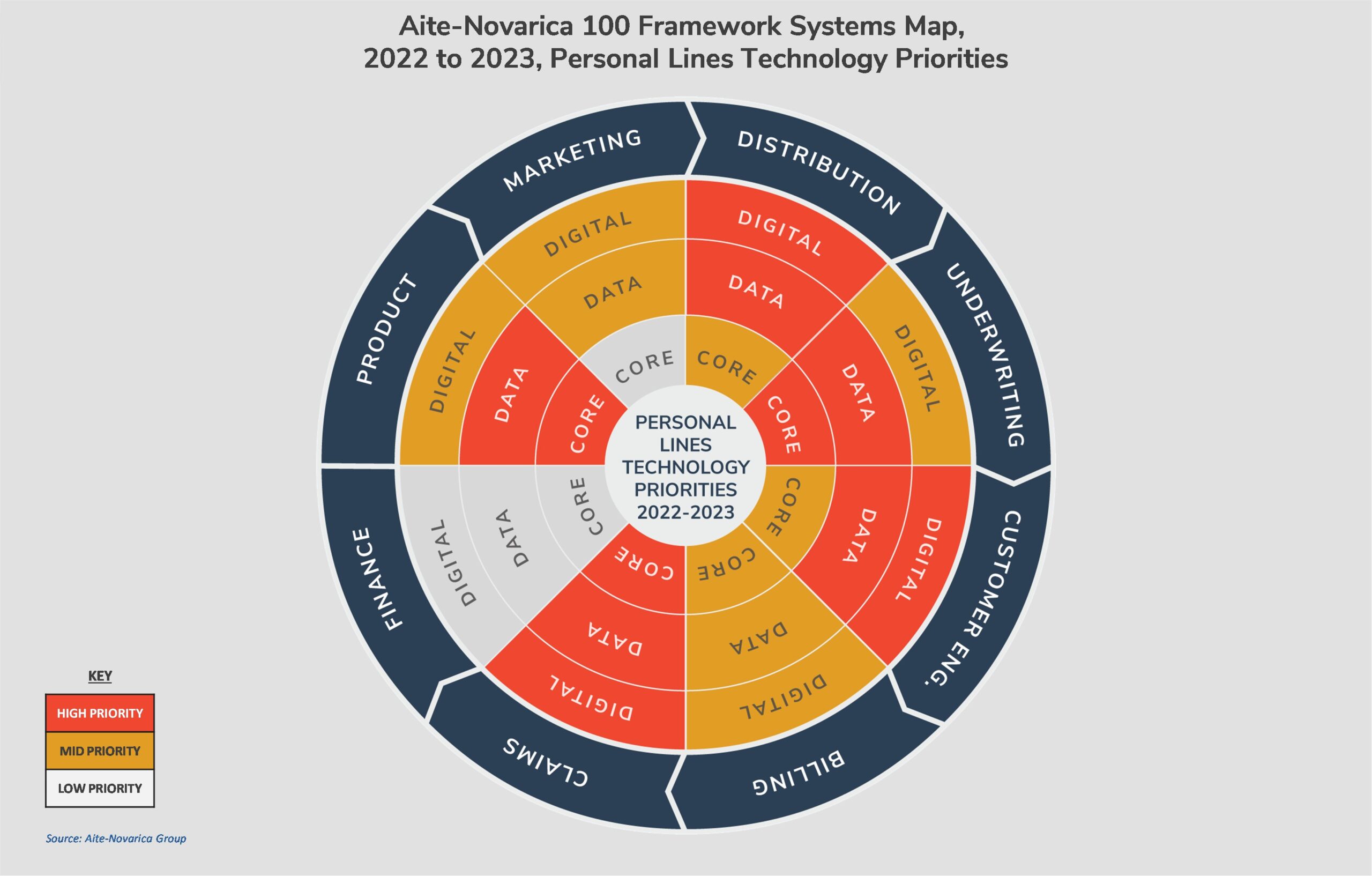

This 37-page Impact Report contains one figure and two tables. Clients of Aite-Novarica Group’s Property & Casualty service can download this report and the corresponding charts.

This report mentions 21st Century Auto Insurance Company of New Jersey, 21st Century Indemnity Insurance Company, 21st Century Pacific Insurance Company, Access Home, AIG, Allstate, Amica Mutual, Arbella Insurance Group, Arity, Berkley Asset Protection, Buckle, California Casualty Group, Carvana, Chubb, Claimatic, Cumberland Mutual, Echelon Insurance, Encova Insurance, Esurance, Everspan Insurance Company, Falcon API, Farm Bureau of Idaho, Farmers, Five Sigma, GEICO, GloveBox, Guidewire, Hastings Mutual, HCI Group Inc., Hippo, HomeX, Incline P&C Group, Kemper, Lemonade, Mercury General, Metromile, Nationwide, Octo Telematics, Onlia, PayPal, Pekin Insurance Group, Permanent General Group, Plauti, Progressive, Root Insurance, SafePoint Insurance Co., St. Johns Insurance Company, Sensa, Sentry Insurance, Shelter Insurance, Slide Insurance Company, Socotra, State Auto, State Farm, State National Fire, Texas Farm Bureau Mutual, Torstar Corporation, United Insurance Holdings, United Property and Casualty Insurance, and West Bend.

About the Author