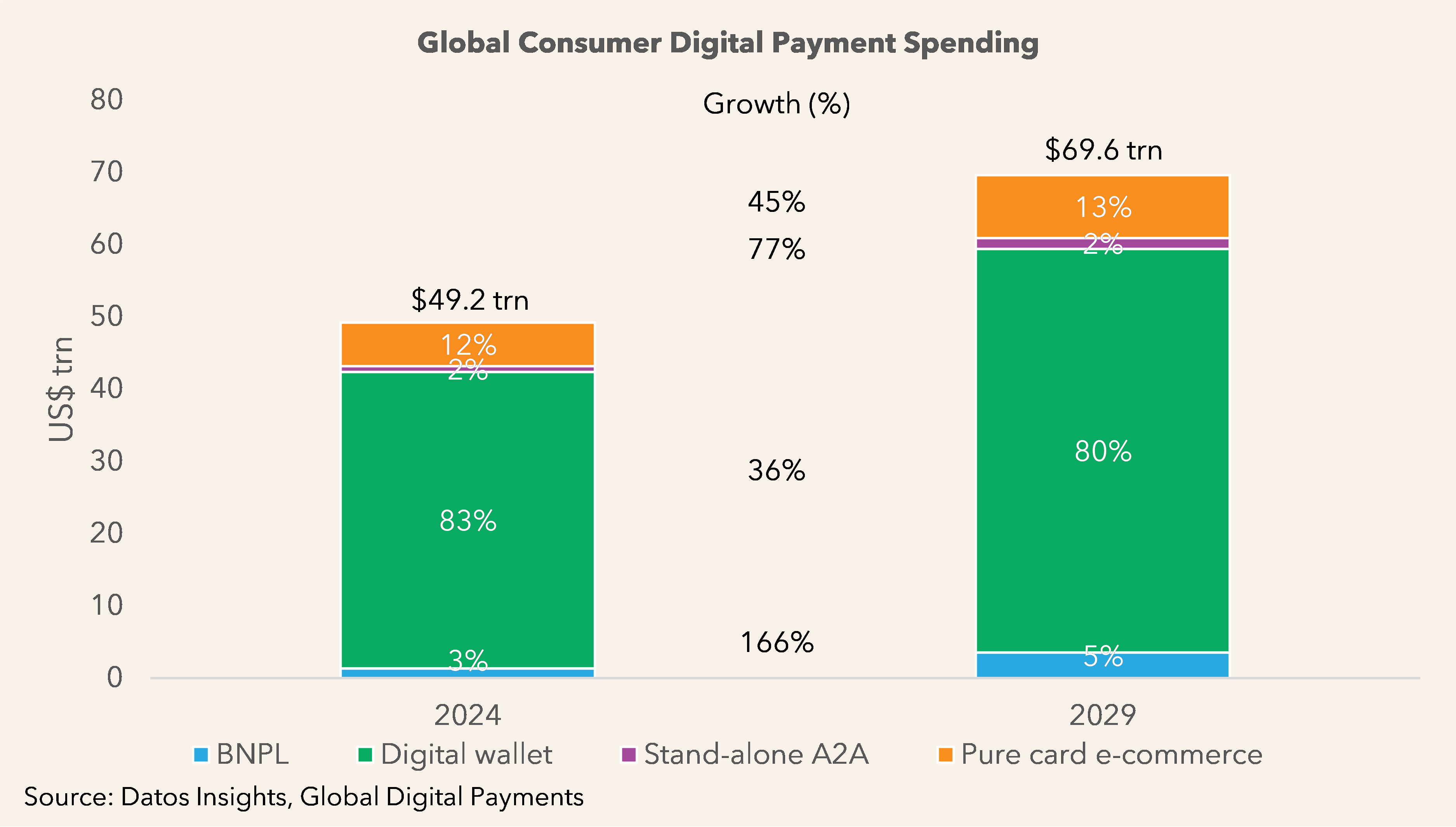

Consumer digital payment spending reached nearly US$50 trillion globally in 2024, with explosive growth of 20% excluding China’s vast and relatively mature digital payments market. These findings come from Datos Insights’ new research, Global Digital Payments.

Wallets hold the lion’s share of global digital payment expenditure

Wallets account for over 80% of all digital payment spending, reaching a staggering US$41 trillion in 2024. They show remarkable versatility, with usage split nearly evenly between in-store and online transactions. Global Digital Payments reveals that regional preferences vary significantly — QR codes are the norm in Asia-Pacific, while NFC technology leads in North America and parts of EMEA.

Wallets are forecast to see 36% growth in spending between 2024 and 2029, but this rises to 126% if China is excluded, just below the level anticipated for Buy Now Pay Later (BNPL), and significantly higher than for stand-alone account-to-account (A2A) and pure card e-commerce.

Alongside the global giants such as Apple Pay, Google Wallet and PayPal, local champions have emerged, such as PicPay (Brazil), PayPay (Japan), Bizum (Spain) and Swish (Sweden). The European Payment Initiative (EPI) plans to begin the P2M rollout of its account-funded Wero wallet in multiple countries from 2025, which is expected to become a major regional player.

BNPL is seeing spectacular growth, but faces headwinds in coming years

BNPL spending soared 21% to US$1.3 trillion worldwide versus 2023, as younger consumers embrace flexible payment options, especially for fashion, electronics, furniture, and travel purchases.

Sweden and Australia lead adoption with 17% and 15% of digital spending respectively, reflecting early innovation by companies like Klarna and Afterpay. While primarily used online (77% of expenditure), in-store adoption varies widely, from 39% of total BNPL spending in Australia to just 2% in the UK.

Global BNPL expenditure is set to almost treble over the forecast period thanks to its flexibility, despite anticipated increased regulation and competition from instalment options on bank cards.

Stand-alone A2A solutions have seen notable success in select markets

Stand-alone A2A consumer spending at merchants grew 13% to US$834 billion in 2024, with solutions like Australia’s PayID, India’s IMPS and the Netherlands’ iDEAL gaining significant traction in their home markets. Meanwhile, Pix has transformed Brazil’s payments landscape, driving both A2A and account-funded wallet spending since 2020. Over 85% of global A2A expenditure is online.

Stand-alone A2A expenditure is forecast to almost double between 2024 and 2029, and to see even stronger growth in markets such as Australia, Brazil and India. Nevertheless, EPI’s plans to replace iDEAL, which it acquired in 2023, with the Wero wallet will moderate A2A growth worldwide.

Pure card e-commerce to be gradually replaced by innovative alternatives

Despite competition from newer methods, pure card e-commerce grew 9% to US$6 trillion. Cards still account for the highest proportion of e-commerce spending in the Americas (68%) and EMEA (52%), though they represent just 7% in Asia-Pacific where wallets predominate.

Cards face gradual displacement by wallets and BNPL, especially among younger consumers looking for innovative ways to pay. Growth in pure card e-commerce between 2024 and 2029 is therefore predicted to be modest, at 45%.

Digital payments will continue to displace traditional methods both online and in store

Digital payment spending is projected to surge to US$70 trillion by 2029 as consumer preferences continue evolving towards frictionless payment experiences.

Daniel Dawson, cards and payments sector lead at Datos Insights commented: “Digital payments are progressively displacing traditional methods across both online and in-store environments. BNPL will continue gaining ground at the expense of credit cards, while wallets will increasingly be favoured over cards of all types, as consumers seek enhanced security, convenience and additional features such as loyalty programme integration.”

Notes to editors

About Datos Insights

Datos Insights is the leading research and advisory partner to the banking, insurance, securities, and payments industries—both the financial services firms and the technology providers who serve them.

In an era of rapid change, we empower firms across the financial services ecosystem to make high-stakes decisions with confidence and speed. Our distinctive combination of proprietary data, analytics, and deep practitioner expertise provides actionable insights that enable clients to accelerate critical initiatives, inspire decisive action, and de-risk strategic investments to achieve faster, bolder transformation.

The information and data within this press release are the copyright of Datos Insights and may only be quoted with appropriate attribution to Datos Insights. The information is provided free of charge and may not be resold.