The recent developments in global tariff policy are significantly impacting international supply chains. Although banking services are not directly targeted by tariffs, they feel the effects in various ways. For example, ATMs remain a key transactional channel for banks, and ATM manufacturers are now evaluating how current trade dynamics affect their operations, supply chains, and market strategies.

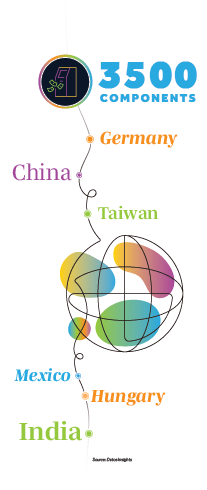

The global ATM industry (valued at approximately $20 to $25 billion) depends on a complex, internationally integrated supply chain. Each ATM comprises over 3,500 components sourced globally—from card readers manufactured in China and display panels in Taiwan to security modules produced in Germany. Final assembly typically occurs in cost-competitive locations such as Hungary, India, and Mexico. This distribution strategy allows manufacturers to meet regional demand efficiently while managing production costs and geopolitical risks.

How ATM Manufacturers Are Adapting to Global Supply Chain Challenges

Given this global supply chain and its specific regional distribution dynamics, a geographic perspective helps us understand the potential impact of tariffs. We must examine the position of U.S.-based manufacturers as well as those in Asia-Pacific, Latin America, and Middle East and Africa (MEA).

U.S.-based ATM manufacturers currently hold around 50% of global market share. This is supported by a network of regionally dispersed production and assembly facilities, which has historically offered cost advantages and reduced exposure to localized trade disruptions.

The Asia-Pacific now accounts for over 55% of global ATM shipments, equivalent to around 160,000 units annually. The region serves as both the largest market and a major manufacturing base. Countries such as China, India, Indonesia, Malaysia, Thailand, and Vietnam are key production locations due to lower labor costs, improving infrastructure, and favorable currency conditions. Asian manufacturers primarily serve domestic and regional markets but are increasingly targeting growth in Europe and MEA. In comparison, the North American market still relies heavily on U.S. manufacturers, while Europe continues to depend on U.S.-based suppliers with established service networks and expertise in meeting local compliance requirements.

Latin America is seeing growing activity in independent ATM network deployments, particularly through joint ventures such as Euronet and Prosegur Cash’s LATM initiative. The region emphasizes cash availability in underserved and high-footfall areas, with an increasing shift toward ATM-as-a-Service models.

In MEA, the focus is on expanding connectivity and improving financial inclusion while integrating newer digital and travel-payment technologies. While both U.S. and non-U.S. international manufacturers are active in the region, local and regional players are becoming increasingly relevant due to their alignment with regulatory requirements and market-specific needs.

Banking Infrastructure at Risk: How Tariffs Are Reshaping ATM Manufacturing

Historically, ATM manufacturers have structured their supply chains to optimize costs and hedge against risks such as tariffs and sanctions. However, the ongoing 2025 tariff war has disrupted this balance, affecting the acquisition of raw materials and the delivery of finished products across key markets. Core materials such as steel and aluminum—critical to ATM production—now face cost volatility and supply uncertainties.

Currently, a 90-day tariff waiver is providing temporary relief, allowing manufacturers to avoid immediate price hikes. Beyond this period, the industry faces significant challenges. While many manufacturers have stockpiled inventory to sustain operations in the short term, uncertainty looms regarding long-term planning. Several leading ATM manufacturers have issued cautious guidance, noting that aggressive cost management strategies may be necessary if tariffs persist or escalate.

U.S.-based manufacturers, despite their global footprint, produce only 10–15% of their ATMs domestically. With the U.S. being the second-largest ATM market globally, new tariffs on imported components or finished goods could substantially increase operational costs. These manufacturers rely heavily on production facilities in Mexico, Eastern Europe, and parts of Asia. Importing finished ATMs back into the U.S. to meet domestic demand could become increasingly expensive.

In response, market players might adopt nearshoring strategies—relocating production to lower-tariff jurisdictions like Canada and Mexico under the USMCA framework. This approach offers partial insulation from U.S.-China trade tensions and aligns with the “eclectic paradigm” (Dunning’s OLI framework), emphasizing location-specific advantages. However, nearshoring doesn’t eliminate cost pressures. Logistical adjustments, labor considerations, and the threat of future bilateral tariffs could erode expected savings.

Strategically, firms face a balancing act between cost optimization and geopolitical risk mitigation. In the short term, rising input costs and regulatory uncertainty may compress margins. Long term, the ability to realign supply chains by reshoring or diversifying component sourcing will define competitive advantage. Ultimately, these shifts may lead to higher costs for banks and consumers as the industry recalibrates.

U.S. vs. Asian ATM Manufacturers: Changing Competitive Dynamics in Banking Infrastructure

All of these challenges may present opportunities for Asian manufacturers. Traditionally focused on non-U.S. markets due to the entrenched dominance of U.S. players in North America, Asian suppliers may find new avenues for growth as U.S. companies shift focus or face cost pressures. Their established presence in Asia-Pacific, MEA, and Latin American—combined with competitive pricing—positions them well to expand in regions where U.S. market penetration could stagnate.

With U.S. players now recalibrating strategies and managing margin compression, Asian firms from China, South Korea, and Taiwan are accelerating expansion into lucrative growth regions such as MEA, Central Asia, and parts of Latin America. Backed by competitive pricing, localized partnerships, and favorable tariff conditions, companies like GRGBanking are making inroads through digital-first offerings and targeted deployments in emerging markets.

While U.S. firms also see non-U.S. regions as growth engines, and many already manufacture abroad, gaining market share is not simply a function of location. Success in emerging markets often hinges on localization, cost competitiveness, and agility in forming public-private alliances. In contrast to their Asian peers, many U.S. players remain structurally focused on high-value segments and premium solutions, which may slow broader regional penetration.

However, the tariff environment remains volatile. For instance, the U.S. has imposed tariffs as high as 174% on select Chinese-made ATM components, including electronic modules and casings. Recent updates as of May 2025 indicate a temporary reduction—such as a 30% rate on Chinese goods (down from 145%) and a 90-day pause on EU tariff enforcement. This highlights the unpredictability that continues to cloud strategic decision-making for manufacturers.

Strategic Implications for Bank ATM Procurement and Management

Given a projected moderate compound annual growth rate (CAGR) of -1% for the global ATM market through 2029, manufacturers must tread carefully. With many players able to manage operations for only 3–4 months using existing inventories, the long-term impact of tariffs will soon become unavoidable.

Key questions arise:

- Will manufacturers absorb these costs?

- Will banks pass them on to end-users?

- Will new players emerge to capture market share from struggling incumbents?

In the U.S., one potential response may be the recycling or refurbishment of existing ATMs. Banks under budgetary pressure may choose to delay new deployments, extending the life of their current fleets instead. This is particularly relevant given that nearly 90% of upcoming ATM shipments are expected to be replacements, not new installations. Price increases due to tariffs may further incentivize banks to hold off on upgrades, which could significantly impact manufacturers—especially smaller players with limited resilience.

If large manufacturers succeed in cutting costs or streamlining operations without affecting end-user pricing, they may emerge stronger, further consolidating market share. In contrast, smaller firms may find it difficult to navigate rising costs and supply chain challenges, potentially leading to market exits or acquisitions.

Implications for Financial Institutions

For banks and credit unions, these supply chain disruptions and potential cost increases come at a challenging time. Many financial institutions (FIs) are already reevaluating their physical channel strategies amid digital transformation initiatives. The possibility of increased ATM acquisition and maintenance costs could accelerate branch rationalization efforts and push more investment toward digital alternatives.

FIs should consider:

- Extending maintenance contracts on existing ATM fleets to delay replacement cycles

- Exploring ATM-as-a-Service models that shift capital expenditure to operational expenditure

- Evaluating alternative vendors, potentially including Asian manufacturers with competitive pricing

- Accelerating the transition to more advanced, multifunctional ATMs that deliver greater value despite higher costs

The timing and implementation of these strategies will be crucial for maintaining service levels while managing costs in an uncertain environment.

Strategies for Banking ATM Networks Amid Supply Disruption

The current tariff environment has created a climate of uncertainty for the global ATM industry. While some manufacturers may find strategic opportunities amidst disruption, others face mounting pressure to adapt. Tariff volatility, combined with modest market growth and rising material costs, is testing the resilience and agility of industry players.

As banks weigh the costs of new ATM deployments against operational constraints, and as manufacturers consider reshoring or rebalancing their global supply chains, the competitive dynamics of the ATM industry may undergo significant realignment. Whether this results in strengthened dominance by major U.S. players, or inroads by emerging Asian competitors, the coming months will prove decisive.

Our next Datos Insights Situation Room on Thursday, May 29 is on “Tariffs, Turmoil, Trust—Engaging Clients in Volatile Markets.” You can also access our recent on-demand recording on the topic, “Tariff Tsunami – Minimizing Fallout While Maximizing Opportunity.” Join us for this collaborative discussion and access to our collective expertise as you navigate these complex market dynamics.