In part one of this blog series, I provided an overview of what life-cycle banking is and how it works in practice. In this second installation of my blog series, I will explore what this looks like when applied across the supply chain.

A supply chain is a network of relationships between different entities that create and deliver products or services. Every company, no matter its size or scope, plays multiple roles in a supply chain: It buys inputs from other suppliers, it produces outputs for other buyers, and it sells goods or services to end customers.

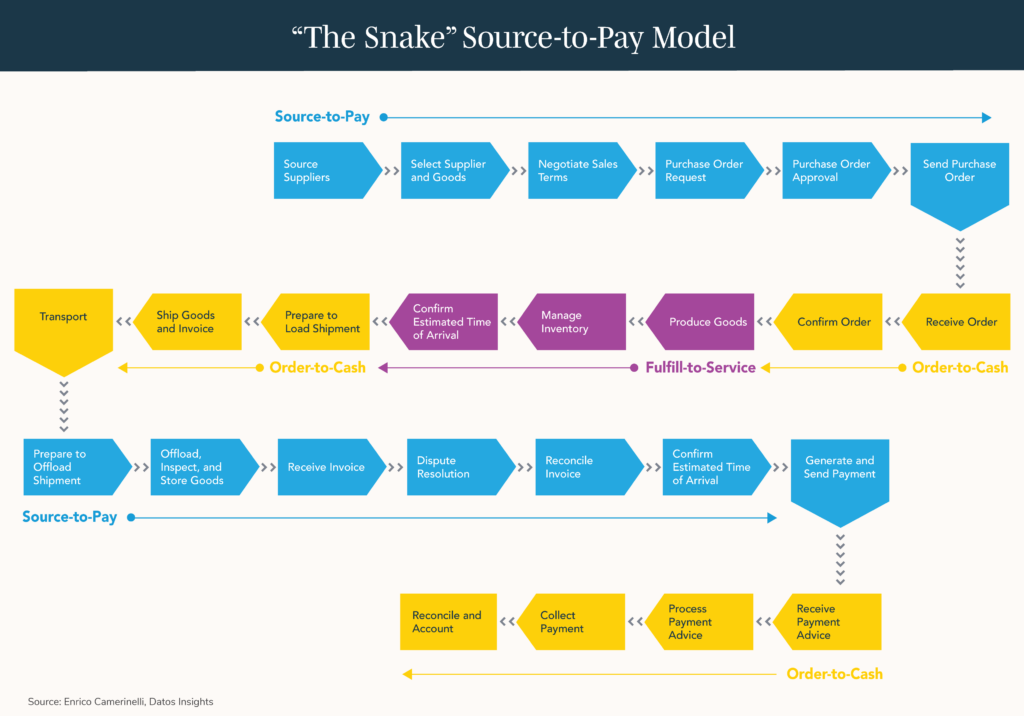

To show the complexity of supply chains, I use a graphical representation I am calling the “snake” because of its shape.

Figure 1: The “Snake”

A snake has different parts that work together to move and survive. Similarly, a supply chain has different components that coordinate to deliver products and services. A more accurate way to describe the components of a supply chain is to use the word “processes”. The processes are the steps that usually occur in any supply chain, regardless of the location. They are represented by the arrowed blocks in the snake diagram.

Source-to-Pay is a category of processes that a manufacturing company uses to purchase goods or services from a supplier. It includes activities such as finding suppliers, negotiating contracts, ordering materials, and paying invoices. Automotive, electronics, and aerospace are examples of heavy users of Source-to-Pay processes.

When a company receives a purchase order from its client, it becomes a supplier for that client. The supplier then has to fulfill the order and collect the payment from the client. This is known as the Order-to-Cash process, which covers all the steps from receiving an order to getting paid for it. The company’s production facilities handle the Fulfill-to-Service operations. This is where the products are made, stored, and packed for delivery to the customers, as illustrated by the diagram.

The Source-to-Pay category involves the processes that the company performs as a buyer when it receives goods from its suppliers. After the goods are delivered, the company verifies their quality and quantity, and then pays the supplier according to the contract terms.

The process of paying for goods involves several steps. First, the buyer takes delivery of the goods and checks their quality and quantity. Next, the buyer receives the invoice from the supplier and verifies its accuracy. If there is any discrepancy or disagreement, the buyer and the supplier need to resolve it before proceeding. Finally, the buyer issues and sends the payment to the supplier according to the agreed terms. The final step of the Order-to-Cash process is when the supplier gets paid by the customer. The supplier then has to record and match the payment with the invoice in the company’s account.

Where Life-Cycle Banking Fits In

In summary, the “snake” illustrates the common processes in a business’s supply chain. You might be wondering: What’s next? How does this relate to life-cycle banking? Let’s review the concept of life-cycle banking: Life-cycle banking provides financial supply chain (FSC) solutions triggered by physical supply chain (PSC) events.

There are two important keywords here: “triggered” and “events”.

The physical supply chain events are the actions that take place in the real world to produce and deliver goods to customers. The financial supply chain capabilities are the tools and processes that enable a company to manage its cash flow, payments, and risk along the PSC. They include things like invoice financing, trade credit, and supply chain insurance. The snake diagram helps to visualize how the physical and financial supply chains are connected and how they affect each other.

A purchase order, an invoice, and a payment are examples of business processes that involve people in the company. These processes are “physical” because they can be done by hand and on paper, as they were in the past. Some companies still use manual and paper-based methods for these processes.

The “snake” metaphor helps us understand how a process flows from one step to another. Sometimes, a process needs some extra services that are not available internally. These services can be provided by external sources, such as financial institutions or fintech vendors. The financial supply chain is a term that refers to the activities and services that external sources provide to support the supply chain. For instance, when a company wants to source suppliers for its products or services, it may require some additional help from outside parties. This could include financing, insurance, logistics, or legal assistance. These are examples of the supporting activities that belong to the FSC.

Examples of Events Triggered Along the Supply Chain

Market intelligence, for example, is a service that provides information about a company’s performance, reputation, and strategy. It can help businesses make informed decisions when sourcing a new supplier. The need for a market intelligence scan arises when a business faces a challenge or an opportunity in the market. This is a “trigger”.

Market scan is the triggered service that helps buyers find the best suppliers for their needs. It is activated (i.e., triggered) when the buyer starts the “Source Suppliers” process in the supply chain. The service can be provided by different types of providers, such as banks, consultants, or fintech companies. The service is integrated (i.e., embedded) with the supply chain process and delivered at the time in the buyer’s life cycle when they are sourcing a new supplier.

One of the other steps in the snake model is to assess the financial risk of the supplier during negotiation. This involves evaluating the probability and impact of adverse events that may affect the supplier’s ability to fulfill the contract terms. Financial risk analysis can help the buyer make informed decisions, quantify risks, and protect their interests. Some of the tools and methods for financial risk analysis that can be triggered at this time include credit scoring, cash flow analysis, ratio analysis, scenario analysis, and simulation. By conducting a financial risk analysis, the buyer can determine the level of risk exposure and the appropriate risk mitigation strategies for dealing with the supplier.

Fast forward: when the buyer’s purchasing department issues a purchase order, it means that they will pay the supplier in the future. This is a cash outflow for the buyer. The buyer’s treasury department needs to know how much cash they will have at that time in the future. This need triggers a service that can forecast future cash flows based on the purchase orders.

A letter of credit is a financial instrument that may be needed in the same process. It is a guarantee from a bank that the supplier will get paid by the client. Before shipping the goods, the supplier may also want to get pre-shipment finance from financial partners. This is a loan that helps the supplier cover the production costs.

What Does All This Have to Do With Life -Cycle Banking?

To provide the right services at the right time, you need to understand the supply chain you are working with. By knowing the supply chain, you can identify the needs and expectations of each stage and offer services that add value and efficiency.

Life-cycle banking is a new way of providing financial services that are linked to the physical activities and requirements of the user. It uses an API-based platform and a network of partners to offer solutions that are tailored to the user’s daily operations and needs. Life-cycle banking leverages the expertise and insights of the user’s industry and market to create value-added services.

The concept of life-cycle banking has been tested in a few scenarios and proven to be feasible. For example, PaperTrl is a platform that helps construction companies manage and automate their accounts payable (AP) processes. It has recently integrated U.S. Bank virtual card payment capabilities into its platform, allowing users to pay their vendors securely and efficiently. This feature also enables users to earn cash back rewards and reduce fraud risk.

The integration with U.S. Bank will allow PaperTrl customers to automate AP operations from procurement to payment. This includes vendor management, purchasing, receiving, invoice processing, and payments via U.S. Bank virtual commercial cards. Together, PaperTrl and U.S. Bank will help AP departments manage all B2B payments from a single platform.

The Next Level of Banking

Life-cycle banking aims to provide banking services that are tailored to the user’s daily sector-specific business activities and needs. It involves embedding the user’s data and preferences into banking capabilities, such as personalized recommendations, alerts, rewards, and insights.

Life-cycle banking integrates financial services with supply chain management. It allows businesses to access banking functions as service components that are triggered by events in the sector’s physical flow of goods and services. For example, an automotive parts manufacturer can use life-cycle banking to automatically initiate payments, invoices, or loans based on the status of their orders, shipments, or inventory. Life-cycle banking aims to improve efficiency, transparency, and cash flow for businesses and their customers. Such processes are peculiar to the industry sector’s PSC dynamics.

Embedded banking is the integration of banking services into non-banking platforms (e.g., ERP, e-commerce, social media, or mobility). Life-cycle banking is the next level of embedded banking, where banking services are tailored to the specific needs and preferences of customers at different stages of their enterprise process cycle. It leverages the data exchanged in banking transactions to create personalized and contextualized offerings that enhance enterprise value. To learn more about the role of life-cycle banking, please read my recent report The BaaS and Embedded Finance Ecosystem: A Reference Framework or my recent blog A New Approach to Sustainable Supply-Chain Finance. And stay tuned for the full version of the snake diagram, which will be published as a free report.