A recent Datos survey on check positive pay, conducted in March 2025, found that more than 90% of U.S. financial institutions state they have seen a rise in the number of fraud attacks against their business/corporate customers over the last year. While the number of checks is decreasing compared to the total number of payments, the value of checks is increasing, as is the gap between attempted fraud and actual losses. With only 29% of U.S. FIs stating they are satisfied or very satisfied with their current positive pay adoption rates, what can FIs do to reduce fraud while increasing positive pay adoption?

Financial Institutions Are at an Inflection Point

Banks and credit unions should no longer consider positive pay services optional or reactive. FIs have been too complacent regarding client relationships, fee sensitivity, and positive pay services. Nearly three-fourths (74%) of FIs require positive pay only after the client has been a victim of fraud. Instead, FIs should require positive pay before fraud occurs. The benefits far outweigh the cost, but customers feel it is a nice-to-have vs. a must-have, with 32% saying their company doesn’t need it. The better approach is ramping up campaigns and education for both clients and internal staff, including relationship managers, treasury sales officers, and front-line team members to ensure clients understand the value of positive pay.

Growing positive pay adoption will lead to additional revenue for FIs, deepen client relationships, and better position FIs to cross-sell other products. Positive pay, in many cases, is the initial add-on service for commercial and SMB clients. It is the logical next step for true business banking account holders, as positive pay can be positioned as either a deposit add-on product or a treasury service, especially when extending to ACH positive pay.

Banks Need to Continue Improving Client Experience

Traditional check positive pay requires business users to provide a daily file or document with details of every check it has issued that day to the bank. The bank compares this information with the checks presented for payment and looks for discrepancies.

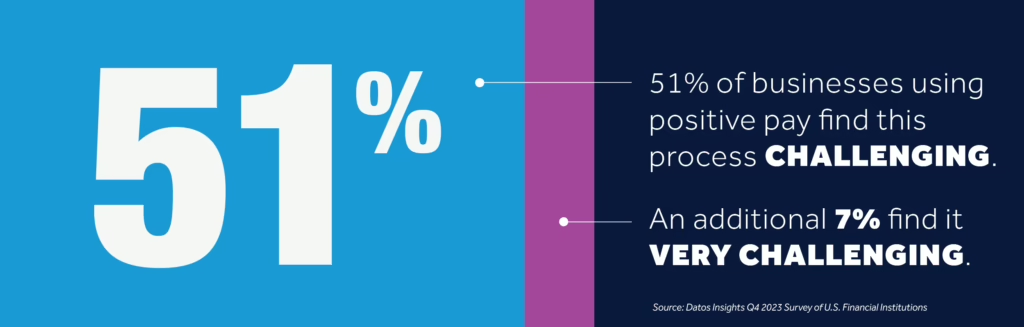

This is a source of friction for both commercial and SMB customers. Corporate treasurers identify integration with accounting systems and ease of file upload as areas in which positive pay is challenging. In the SMB segment, uploading a check issue file is practically nonexistent since the number of checks is marginal. Even when offering reverse positive pay, without payee name or check serial matching, SMBs are more exposed than their corporate peers.

Adding tools like API connectors to accounting platforms to automatically sync issue files or adding integration with existing services like accounts payable, bill pay, or payroll platforms that automatically sync check payments with outstanding check issue files would greatly reduce the friction of manually uploading and approving files.

Artificial Intelligence and Data Enrichment

Looking forward, FIs and technology providers must invest in enhancing their products to make using positive pay easier and more effective, especially in the SMB segment, in which 91% of businesses that are currently using but not paying for reverse positive pay would be willing to pay for it.

When using reverse positive pay, one of the biggest limitations—besides the linear item review process—is that clients only have the check number to review. With check washing and check theft, the amounts and names are replaced.

The solution is to leverage AI and data enrichment to create a better experience and one that is integrated into information reporting without having separate modules for positive pay:

AI: Character recognition exists today, but AI expands that capability when the payee name information and check serial numbers are known. AI, especially agentive AI, can identify sophisticated fraud patterns, unusual check amounts, and suspicious payee names. Agentive AI can create intelligent exception handling in which items are categorized and prioritized for review.

Data enrichment: The ability to add payee names to transactions and incorporate those into transaction reporting not only simplifies the review process but also provides an additional data point for AI tools to analyze to identify fraudulent items. Imagine reviewing your account and seeing “John & Jane Doe Corp” as the transaction description instead of “Check.”

The problem of under-adoption of positive pay will not correct itself overnight. However, small changes to strategy, product communication, training, and how the product is offered can have an immediate impact and better protect FIs and their clients from the rising threat of check fraud, along with increased recurring revenue for banks. For further resources on positive pay solutions and strategies, please contact Chris Buerkle at [email protected] or visit our website.