Environmental, social, and governance (ESG) products and services within commercial banking have accelerated over the past several years. Many businesses have transitioned from green-agnostic or greenwashers to making real investments toward sustainable initiatives. As sustainability and other ESG-linked goals have reached business leaders’ agendas, banks have begun to offer services and products to help guide their clients as they maneuver ESG improvements alongside other, often more pressing, financial concerns.

As we reach the anniversary of the largest government spending-package geared toward sustainability to date, it’s worth reflecting on where ESG in commercial banking currently stands and where it’s headed in the near term.

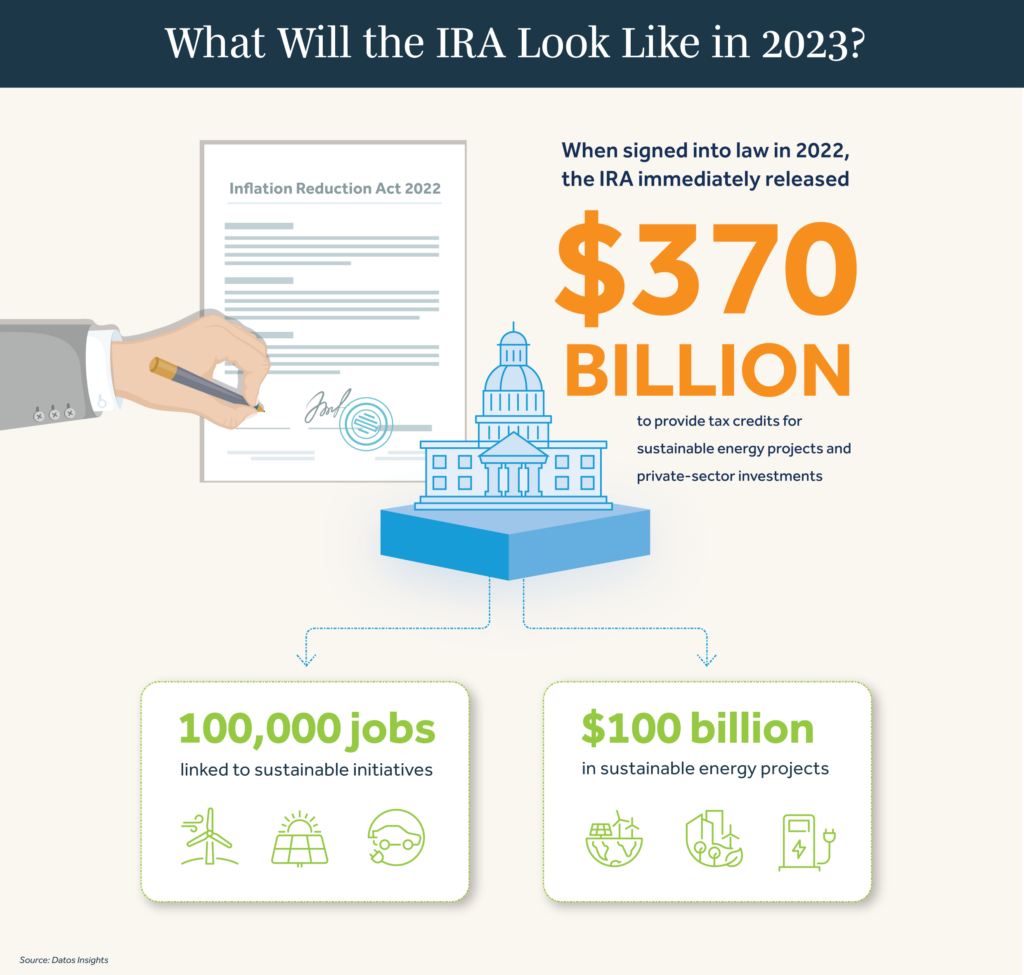

The Inflation Reduction Act of 2022

The Inflation Reduction Act of 2022 (IRA), enacted a year ago, contained new spending programs and tax adjustments aimed at lowering both inflation and the federal budget deficit. The legislation modified existing tax codes, impacted tax enforcement, adjusted prescription drug policies, and further built on existing COVID-19 relief efforts, among many other spending initiatives.

The IRA was also, according to the Department of Energy, the “single largest investment in climate and energy in American history.” Various estimates have placed the combined spend and tax incentivization of the sustainability-linked initiatives in the IRA between US$700 billion and over US$1 trillion through 2030.

Given the IRA’s clear focus on sustainable energy transition, the legislation might as well have been called the Emissions Reduction Act. Most of the total cost for the IRA’s sustainability-linked goals stems from tax credits with the obvious goal: Businesses and individuals will invest in renewable energy sources and make other sustainability-linked improvements if it makes financial sense.

It has only been one year since the passage of this landmark sustainability legislation, so assessing its overall effectiveness or contribution toward substantial reductions in emissions isn’t exactly fair.

When signed into law, the IRA immediately released US$370 billion in funding to provide tax credits for sustainable energy projects and private-sector investments. Within six months, the IRA reportedly created over 100,000 jobs linked to sustainable initiatives, especially within the wind, solar, and electric vehicle (EV) sector, and resulted in nearly US$100 billion in sustainable energy projects.

Targeted tax credits are geared toward the transportation and manufacturing sectors, with specific tax credits for electric trucks, charging infrastructure and equipment for fleet owners, zero-emission equipment at marine terminals, battery storage, and renewable energy sources at manufacturing sites. The IRA has also expanded the tax credit for “green” improvements to existing industrial buildings and new industrial development, including solar panel installation, HVAC improvements, and more. Finally, the IRA has expanded tax incentives for emission offsets such as carbon sequestration.

Judging by job creation, implementation of new sustainability projects, and spurring what appears to be consistent growth in the “green” sector, the IRA has shown considerable signs of preliminary success.

What This Means for Businesses

Businesses in the U.S. were already making sustainable improvements a greater priority. The reasons for this are complicated, but at a high level, the causes for the shift toward sustainability come down to investor demand based on ESG risk assessments, consumers and activists pushing larger companies to take a more active approach toward social goals, and many businesses viewing ESG or sustainability as complementing existing marketing efforts and, in some cases, good for overall business.

Context matters as well. The EU has passed numerous regulatory frameworks advancing ESG and sustainable goals impacting U.S. businesses that directly or even indirectly work in European markets. The Securities and Exchange Commission (SEC) in the U.S. has proposed new regulations, and broader legislation geared toward ESG or sustainability goals is often debated in election cycles.

The outcome of proposed regulatory shifts is still unknown, but regardless, many U.S. businesses assume ESG and sustainability will grow in importance from a business and regulatory standpoint in the coming years.

While many businesses have shifted toward ESG and sustainable initiatives in theory, in practice the outcomes have been somewhat mixed. For many businesses, hurdles to making significant improvements include lack of clear direction, data, and knowledge on how to implement a clear ESG or sustainability strategy, especially when it comes to a company’s broader footprint and supply chain. In addition, the high financial cost of investing in things like solar panels or other significant improvements often means high-impact improvements never make it past the proposal stage.

The IRA helps with some, but not all, problems for businesses seeking to make ESG and sustainability improvements. The legislation does not make clear what sorts of oncoming regulations businesses should begin preparing for, nor does it help businesses better understand or utilize ESG data, implement a clear ESG strategy, or understand which areas a business should prioritize for improvement.

However, the IRA is helping grow the “green” sector by pushing demand, and it enables businesses to better make a business case for investing in sustainability improvements through tax credits, widening availability of sustainable solutions, and incentivizing carbon capture.

Tax credits will mean more companies pursuing carbon capture and offsets as part of their broader emission reduction strategy, which will result in increased sustainability improvements within commercial and industrial real estate development as well as rehabilitation, manufacturing, and logistics.

Crucially, the financial incentives for sustainability within the IRA have helped or will soon help many businesses begin or expand their ESG roadmap. In order to help establish or broaden an ESG roadmap to go beyond utilizing tax credits, businesses may need a partner to help guide ESG and sustainability improvements, which often comes through an ESG consultancy provider. Financial institutions (Fis) have begun expanding their ESG scope, going from bank disclosure reporting to also including ESG products and services within commercial banking, often expanding and building upon early-stage ESG strategies.

Commercial Banking and ESG

Datos Insights research has shown that roughly 60% of commercial end users are interested in utilizing ESG products and services through their FI. Banks already have experience navigating ESG within capital markets and wealth management, and many banks make annual disclosures on ESG performance to align with various non-governmental reporting standards.

Along with disclosures and reporting, some banks have made net-zero commitments and have accelerated their own ESG strategies, clearing the way for these institutions to make significant improvements over the coming years. Banks engaged in making significant steps toward sustainability and other ESG improvements have acquired experience and expertise, making them valuable partners for businesses seeking to do the same.

For most businesses, borrowing money is necessary to make significant sustainability improvements. Some FIs have begun offering “green loans” with favorable terms for businesses investing in things like renewable energy. Banks can also offer products and services that reduce paper usage within financial processes, such as digital payments and paperless invoicing, among many others.

Reducing paper consumption and adding solar panels is a great starting point for many businesses, but if a business wants to confront its broader supply chain footprint, then aligning with its FI becomes even more critical.

Banks have access to payments and other transaction data, producing what amounts to a broader map of a business’s entire ecosystem. Banks can offer products and services taking advantage of this type of data for reporting, assessments, benchmarking, compliance, and even as tools for promoting downstream influence, such as offering preferable payment rates to suppliers with improved ESG performance or integrated carbon offsets within business-to-business payments.

The IRA and Commercial Banking

The extent to which commercial banking divisions offer ESG products and services varies widely throughout the U.S. banking landscape. Put broadly, the entire market is relatively new and immature. A bank may offer a commercial card with carbon offsets for travel purchases but then fail to tout some of the environmental benefits of digital payments on its website.

Some banks already offer businesses help with ESG reporting but then have no plans to consider ESG supply chain analysis tools. Green lending is perhaps the most common ESG product within commercial banking, and even that is not ubiquitous throughout the industry.

Yet even with an immature market, demand for ESG products and services is growing across companies of differing geographies, revenue sizes, and industry verticals, and companies want their banks to help them achieve ESG-related goals. Especially if the SEC implements new regulations, many businesses and their banks are unprepared to meet new ESG challenges, primarily because of the challenges associated with making a strong business case for developing and onboarding new ESG solutions.

The IRA helps make the business case for banks to either newly enter or further develop ESG offerings within commercial products and services. The demand for ESG products and services already exists and is likely to grow. New regulations are likely to come in the near or midterm.

Even through continuous warning alarms of an oncoming recession, through interest rate hikes, and with a tech sector that has seen continuous shake-ups in the recent past, the “green” sector is growing quickly, in part due to the ever-growing reality of climate change, but also because of the sustainable initiatives in the IRA.

Final Thoughts

Banks are uniquely poised to become leading partners for businesses of all sizes seeking to meet regulatory shifts and accelerate ESG and sustainability-related goals. The IRA has presented an opportunity for banks to enter the ESG commercial banking market or mature existing ESG products and services.

FIs can begin by publicizing their existing ESG disclosure processes, year-over-year improvements, and make or highlight sustainability goals for 2025, 2030, and beyond.

Further entry into the ESG commercial banking market means educating clients on the sustainable benefits of existing initiatives, such as digital payments and paperless processes. ESG preparedness requires training relationship managers on how to have conversations about ESG with clients and integrating ESG into cross-sell opportunities. Especially as banks transition from market entrants to market leaders, they will need to develop or create fintech vendor partnerships to roll out specialized and impactful ESG products.

Some solutions to consider include a green lending program with vertical knowledge in solar, wind, and geothermal; green deposit accounts for businesses; commercial card programs with carbon offsets; access to reporting and disclosure services; cash management and supply chain ESG analysis tools; and integrated mechanisms for carbon offsets within payments.

As ESG grows in importance within commercial banking, investing now in varied solutions, training, and industry specialization avoids loss of market opportunity going forward and can provide banks with a competitive edge through problem solving for clients as they face new and unique challenges. For more information on ESG in commercial banking, see some of my recent reports or reach out to me at [email protected].