Two-thirds of Americans live paycheck to paycheck, only 27% are paid weekly, and 25% are gig workers with irregular income. Banks see it in customer accounts and haven’t fixed it. BNPL users aren’t fringe customers but primary banking relationships solving a cash-flow need elsewhere. Affirm has applied for an FDIC charter, and Klarna has 5 million consumers on a debit card waitlist: For every month banks wait, fintechs deepen these relationships further.

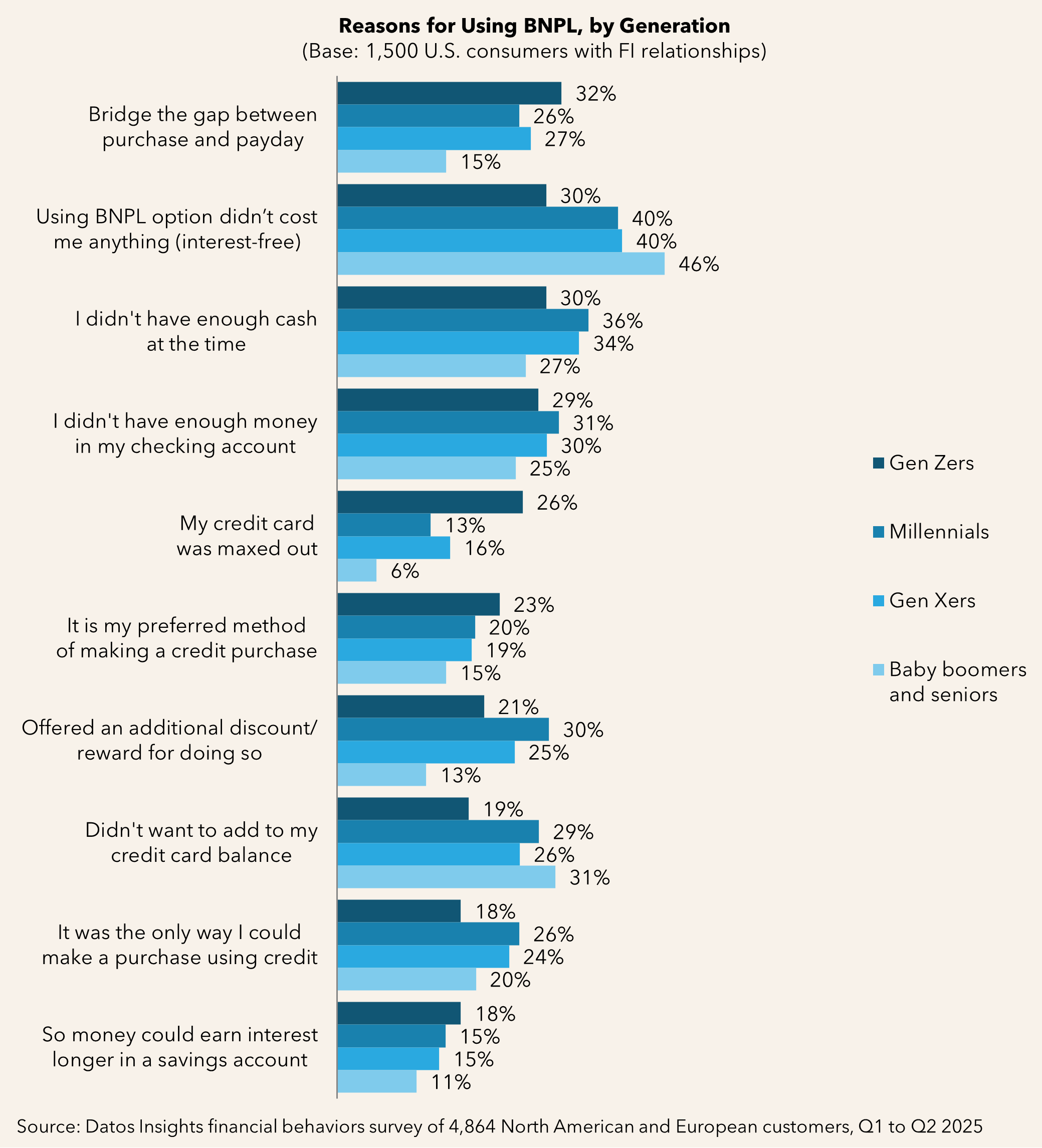

Datos Insights identifies two distinct BNPL segments: the cash-flow manager and the financially stretched consumer. Both live in bank portfolios now. Banks already outperform fintechs on BNPL customer satisfaction. However, existing cash-flow solutions are not closing the gap because the product gap, not the trust gap, is what is keeping banks behind.

This report maps which customers are at risk, identifies the product gap, and outlines how to close it with DDA-anchored cash-flow solutions. The payoff: higher debit interchange, deeper digital engagement, and primary relationships defended before fintechs make them permanent. It is based on three waves of Datos Insights’ U.S. consumer research, including a study of 4,864 consumers in the U.S., Canada, and select European countries conducted in Q1 to Q2 2025.

Clients of Datos Insights’ Retail Banking & Payments service can download this report.

This report mentions: Affirm, Afterpay, BankAmericard, Chime, Current, Diners Club, equipifi, Fiserv, Klarna, Mastercard, PayPal, Peach Finance, Varo Bank, Visa, and WebBank.

About the Author