Boston, October 28, 2020 –These are peculiar times for banks and FIs that lend money to businesses: the pervasive adoption of digitalization demanded by the COVID-19 pandemic, low interest rates, and an oversupply of capital. But business lending is far more than a profit center, as it often forms the tip of an FI’s spear: It forms an entry into a business from which a bank can cross-sell far more profitable services. Before all that terrific cross-selling can happen, commercial loans must be originated, and therein lies the rub. CLO requires the completion of many complex tasks involving financial analysis, deal structuring, proposal writing, proposal distribution, and the acquisition of approvals by credit authorities.

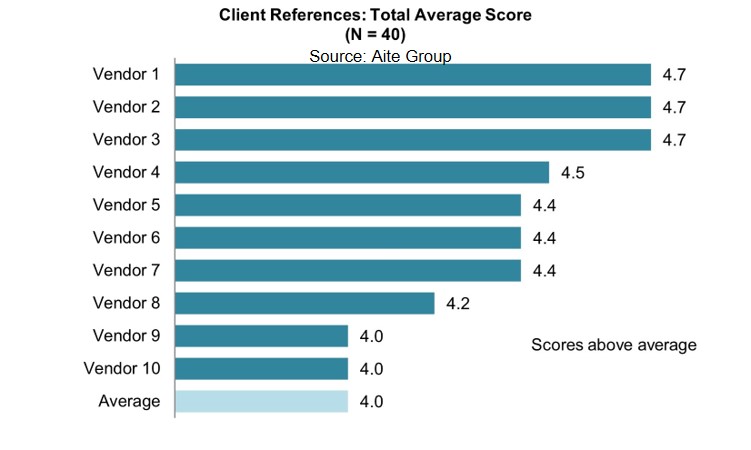

This Impact Report explores the perspectives of clients actively participating in this vendor market and highlights some of the key drivers for clients seeking vendor solutions, various reasons for specific vendor selections, and client views across a number of essential capabilities of each vendor. Leveraging the process laid out by the Aite Matrix, a proprietary Aite Group vendor assessment framework, this report provides views of client references related to the CLO market.

This 33-page Impact Report contains 17 figures and two tables. Clients of Aite Group’s Wholesale Banking & Payments service can download this report, the corresponding charts, and the Executive Impact Deck.

This report mentions Abrigo, Baker Hill, Finastra, FIS, Global Wave, Intellect Design Arena, Jack Henry & Associates, Moody’s Analytics, Newgen Software, Nucleus Software, Oracle, and Q2.