As individuals and businesses returned to international travel and increasingly shopped online at foreign retailers, global cross-border spending grew by 23% last year

Cross-border share of total card spending rises to 6%

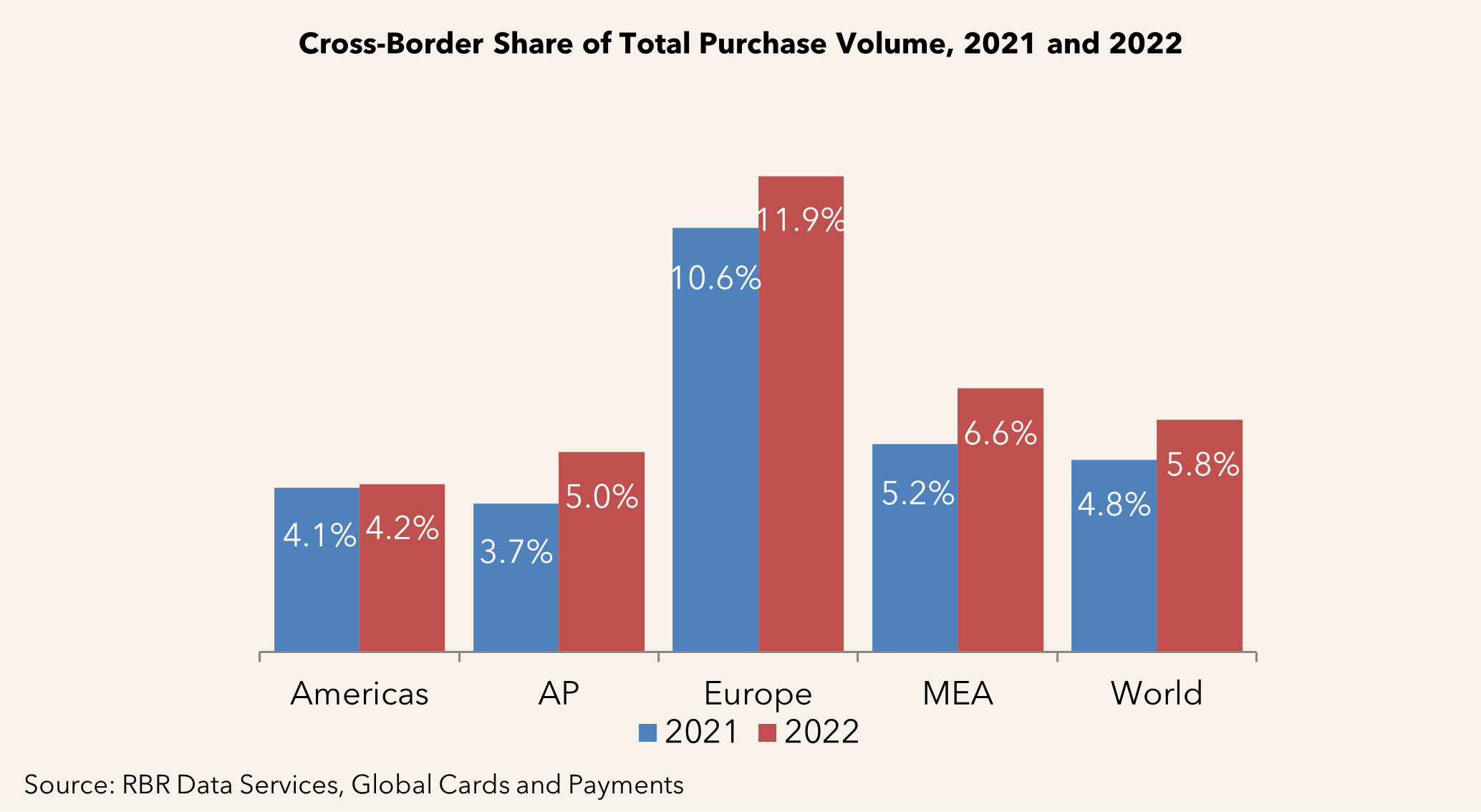

New research from RBR Data Services, a division of Datos Insights, reports that 6% of all global card volume was cross-border in 2022, up from 5% the year before. With the pandemic over and travel restrictions lifted, consumers have been keen to book trips abroad again. In addition, businesses have returned to in-person international meetings and conferences, despite the growth of virtual meetings and events during and since the pandemic.

E-commerce payments, which were boosted during the pandemic, are continuing to be driven by globalisation, with consumers increasingly shopping at online marketplaces based outside of their home countries.

Credit card issuers are offering more and more travel-related benefits

Global Cards and Payments shows that while debit cards make up approximately half of all cross-border spending, credit cards are accounting for a growing proportion, as issuers are expanding the benefits offered on T&E credit products, such as fee-free overseas payments.

As many prepaid products are gift cards, they are often used to make e-commerce purchases, many of which are cross-border. However, due to the prepaid sector’s relatively small share of global card spending overall, its share of cross-border spending also remains low.

Bulgaria and Singapore stand out with particularly high cross-border card spending

RBR’s study reveals that the cross-border share of total purchase volume is highest in Europe, where 12% of all card spending was either carried out abroad or at foreign online merchants. In Bulgaria, cross-border spending is especially high, with consumers tending to use cash for day-to-day domestic purchases, but switching to card payments when abroad.

Almost half of the world’s cross-border card spending was made on cards issued in Asia-Pacific, with Singapore’s cross-border share of total purchase volume being the highest in the region. Not only do Singaporeans often use cards when visiting neighbouring countries like Malaysia and Thailand, but they regularly make online purchases at foreign retailers, such as those based in India. However, a real-time link facilitating simpler cross-border money transfers between Singapore’s PayNow and India’s UPI was launched in February 2023, which could limit future growth in cross-border card spending between the two countries.

There is relatively little cross-border spending in the USA (and none at all in Iran)

According to RBR’s research, while the UAE’s status as a regional commerce and finance hub means that cross-border spending has a relatively high share of overall card volume in this market and in the region as a whole, this is not the case for every country in the region. Cross-border payments are not possible on Iranian-issued cards, all of which are domestic-only, and none of which have acceptance agreements with other countries.

The cross-border share of total purchase volume is lowest in the Americas region, at just 4%. While Canadian consumers and businesses often make in-person and online payments in the USA, cross-border payments are rarely made by US citizens themselves, largely due to the strength of the country’s domestic T&E and e-commerce sectors.

Cross-border card spending is set to keep rising, despite competition from alternative products

Daniel Dawson, who led RBR’s Global Cards and Payments study, commented: “While it was largely due to the easing of travel restrictions that cross-border card spending rose significantly in 2022, growth momentum will continue over the coming years. Not only are consumers becoming increasingly confident making card payments abroad, but purchases at foreign online stores are on the rise.”

With cross-border card spending forecast to grow in the coming years, so too is the scale of alternative payment solutions that can be used at foreign merchants. While such alternatives are a genuine threat to card payments, card issuers are not standing still and increasingly focusing on launching products that are convenient for cross-border spending to combat such threats

Notes to editors

About RBR Data Services

RBR Data Services provides clients with independent and reliable data and insights through published research, consulting and bespoke data services. Our global research covers the cards and payments, retail technology and banking automation sectors and is used by the leading market participants, analysts and regulators as the authoritative source of industry and competitor benchmark data. For any questions about this release, please contact [email protected].

About Datos Insights

Datos Insights delivers the most comprehensive and industry-specific data and advice to the companies trusted to protect and grow the world’s assets, and to the technology and service providers who support them. Staffed by experienced industry executives, researchers, and consultants, we support the world’s most progressive banks, insurers, investment firms, and technology companies through a mix of insights and advisory subscriptions, data services, custom projects and consulting, conferences, and executive councils. Visit us on the web and connect with us on LinkedIn.

Press Contact:

Kaitlyn Labbe

Public Relations

+1.857.327.9442

[email protected]

The information and data within this press release are the copyright of Datos Insights and may only be quoted with appropriate attribution to Datos Insights. The information is provided free of charge and may not be resold.