Commercial insurance is characterized by complex coverages, heterogeneous exposures and risks, and individually negotiated and priced contracts. Distribution is often through independent agents and brokers; there is an involved sales process of negotiation between policyholder, agent, and insurer.

Commercial lines insurers continue to raise rates, seek growth through expanded jurisdictions and new products, and are adopting AI and analytics more broadly. Insurers want to drive down the cost of service, refine pricing and underwriting, and pursue growth.

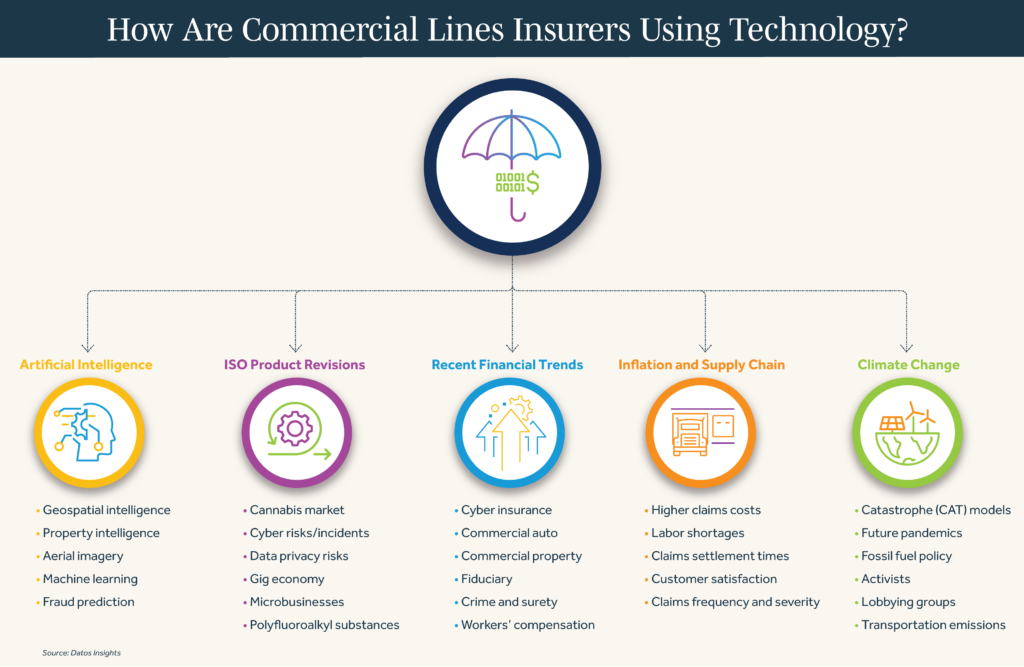

Increased Use of Artificial Intelligence (AI)

Commercial lines insurers continue to use AI and machine learning for use cases ranging from contractor insurance verification and customer experience to claims and underwriting. The number of companies using geospatial and property intelligence solutions to better assess underwriting risks continues to grow. Given the previously mentioned impacts of climate change, more companies are leveraging aerial imagery and machine learning to determine more accurate pricing for the insured exposures.

The use of AI for the ingestion of unstructured text for use in claims and underwriting is becoming more common. Insurers’ investments in data availability and AI-enabled decisioning are letting them streamline or fully automate formerly time-consuming processes for loss-run ingestion, submission intake, and transaction clearance.

Insurers are also using AI and analytics to determine next best actions in claims. Starting with first notice of loss, carriers are able to triage the claim for adjuster assignment, ingest damage photos, estimatics, and payment. Claims fraud continues to challenge the industry as fraudsters seek more sophisticated mechanisms to take advantage of insurers. AI helps to combat fraud by continuously learning new patterns from a variety of data sources and generating a fraud prediction score. Insurers are benefiting from AI to identify provider fraud rings across claims as well as claims that are completely fraudulent.

In evaluating potential intelligent document processing solutions, insurers should consider whether to pursue a horizontal solution, fit-for-purpose solution, or platform component, which will subsequently dictate how broadly applicable the solution will be, how long it will take to achieve value in the form of accurate results, and how easy it will be to tie the solution into the rest of the insurer’s ecosystem.

Insurers are beginning to explore the possibilities of generative AI and large language models (LLMs), with use cases including basic research, chatbots, and policy language interpretation. Insurers should ensure they have basic data and analytics capabilities, data governance, and a data strategy in place before chasing the newest technology. They should also ensure that they can demonstrate the fairness and transparency of their AI processes to various regulators. With these foundations in place, insurers can more comfortably deploy value-added, AI-enabled solutions throughout their organization.

The number of insurers using AI and related technologies to extract data from documents in multiple formats for loss runs, new business, and renewal submissions, and passing that data into core underwriting systems through API integration or robotic process automation continues to increase along with the number of solution providers offering these capabilities. Insurers should consider whether they want to deploy horizontal solutions, fit-for-purpose solutions, or platform components.

ISO Product Revisions

Verisk regularly makes updates to ISO commercial insurance forms, loss costs, and rules to help commercial insurers keep their programs aligned with today’s realities. ISO programs already address the cannabis market, cyber risks, data privacy risks, the gig economy, and microbusinesses. ISO recently revised its general liability coverages to offer exclusionary endorsements for Perfluoroalkyl and Polyfluoroalkyl Substances (PFAS), data privacy regulation violations, and cyber incidents, as well as optional buy-back endorsements for coverage of bodily injury or property damage as a result of cyber incidents.

Other recent revisions include optional exclusionary endorsements for businessowners, commercial auto, commercial property, and crime/fidelity; for businessowners, related rules, and loss costs for microbusinesses with zero to four employees; for commercial auto, a new class plan/rules manual to improve risk classification, updated loss cost filings for hired auto liability and physical damage and auto dealers liability; and for commercial property, a mandatory exclusion of cyber incidents with an exception for loss or damage caused by fire or explosion, a California-specific rule on availability and application of credits for insureds’ wildfire mitigation risk characteristics, and an optional endorsement to provide cannabis coverage where cannabis is legal.

Verisk ISO also plans new and updated classifications, rules, endorsements, and coverages for commercial general liability; a potential commercial auto exclusion for cyber and coverage for operational data outside cyber; a commercial property exclusionary endorsement for risks from solar flares or other space weather; an optional exclusionary endorsement for loss or damage to covered property caused directly or indirectly by space weather, regardless of any other cause or event that contributes concurrently or in any sequence to the loss; optional exclusions for non-fungible tokens and electronic currencies; and new and updated classifications, forms, rules, endorsements, and coverages for businessowners.

Recent Financial Trends

MarketScout reported in Q2 2023 that the average commercial lines rate increase was 5%, with the highest rate increases in cyber insurance, commercial auto, and commercial property. The smallest rate increases were in fiduciary, crime and surety, and workers’ compensation.

Inflation and Supply Chain Constraints

High inflation and the war in Ukraine have continued to affect supply chains, resulting in higher claims costs, from replacement parts for commercial auto to rebuilding and repair costs for commercial property. In addition to materials costs, labor shortages have affected commercial auto and commercial property. Labor shortages and supply chain constraints also lengthen claims settlement times, reducing customer satisfaction. Insurers have been raising rates on commercial auto policies, though it is unclear whether this will be sufficient to address rising loss costs. A shortage of truck drivers, exacerbated by increasing retirements and moves to hire younger replacements, affects claims frequency and severity.

In addition to wage and price inflation, insurers are experiencing increased claim costs due to social inflation, driven by shifts in societal attitudes toward litigation and larger jury awards and an overall negative perception of large corporations. Talent shortages continue to affect carriers (as experienced employees retire) and the businesses they insure. Less experienced business employees can result in poorer quality goods and services.

Firms’ restructuring of their supply chains, including reshoring and related investments in infrastructure and production facilities, will increase demand for commercial insurance. Swiss Re estimates supply chain restructuring will lead to US$36 million in additional commercial premium globally.

Climate Change

Climate change impacts a broad swath of lines of business. Changes in weather patterns mean that insurers can no longer rely upon historical data; they must modify catastrophe (CAT) models. Climate change also increases the chances of tropical diseases spreading to new areas, so insurers must quickly decide how to handle future pandemics.

Insurers have already begun to reduce or end underwriting for fossil fuel companies, a change that European insurers have led. Activists, lobbying groups, and other businesses are pressuring underwriters to accelerate this process. Shipping is an important source of emissions from transportation. The war in Ukraine may be reversing the trend of moving away from the fossil fuel business as countries seek to diversify their sources of fossil fuels. Some state governments are making moves to ban financial services firms from considering environmental, social, and governance factors in their investing strategies and when setting rates. If you’d like to discuss our key findings in the commercial lines insurance space, please read our new report Business and Technology Trends, 2023: Commercial Lines or contact Martina Conlon, Carey Geaglone, or me to continue the conversation.