In this blog, I would like to share some of my recent findings on an innovative concept that I have branded “life-cycle banking”. Life-cycle banking is a new way of thinking about banking services that adapt to the changing needs and preferences of customers based on the industry sector in which they operate.

Life-cycle banking is based on two key trends in the banking industry: Banking-as-a-Service and embedded banking. Banking-as-a-Service is the idea that banks can offer their core capabilities, such as payments, lending, or deposits, as modular and flexible services that can be integrated into other platforms and ecosystems. Embedded banking is the idea that banking services can be seamlessly embedded into the customer journey and context, such as enterprise resource planning (ERP), e-commerce, social media, or mobility.

By combining these two trends, life-cycle banking aims to create personalized and relevant banking experiences that match the customer’s life stage, goals, and preferences. My research explores the benefits and challenges of implementing life-cycle banking, as well as the best practices and examples from leading banks and fintech players around the world.

Life-cycle banking is a possible evolution of embedded banking, where financial services are not only integrated into digital platforms, but also tailored to the specific needs and preferences of customers at different stages of their enterprise business lives. In the first part of this two-part blog series, I will explore how life-cycle banking can be applied to the supply chain of a company and how it can create value for both the company and its suppliers, customers, and partners. In the second part of the series, I will present some likely use cases of life-cycle banking in the supply chain, and discuss the benefits and challenges of implementing them. But before diving into the use cases, let me explain what life-cycle banking is.

A Quick Overview of Life-Cycle Banking

Life-cycle banking is a concept that aims to provide banking services that are tailored to the user’s daily activities and needs. It is based on the idea that banking should not be a separate or isolated activity, but rather an integrated and seamless part of the corporate user’s life.

By embedding the entire knowledge of the user’s day-in-the-life business activities and needs within the offered banking capabilities, life-cycle banking can deliver personalized and relevant solutions that enhance the user’s company financial well-being. In other words, life-cycle banking means day-in-the-life banking capabilities that make banking easy and convenient for the enterprise user.

Day in the life of what? Let’s take the example of a day in the life of a supply chain manager.

What does a supply chain manager do? A typical day for a supply chain manager might start with checking the status of the orders, inventory, and shipments. They might use a dashboard or a software system to monitor key performance indicators (KPIs) such as delivery time, fill rate, inventory turnover, and customer satisfaction. They might also communicate with their team members, suppliers, and customers to coordinate activities and resolve any issues or problems.

Throughout the day, a supply chain manager might also perform various tasks such as:

- Forecasting the demand and supply of products and services based on historical data, market trends, and customer feedback.

- Planning the production, procurement, and distribution of products and services based on the demand forecast and available resources.

- Negotiating with suppliers and vendors to secure the best quality, price, and delivery terms for materials and services.

- Managing inventory levels and locations to ensure optimal stock availability and minimize storage costs.

- Implementing quality control measures and risk management strategies to ensure compliance with safety, environmental, and ethical standards.

- Analyzing data and reports to identify the strengths and weaknesses of supply chain processes and performance.

- Implementing continuous improvement initiatives and best practices to enhance the efficiency, effectiveness, and sustainability of the supply chain.

A supply chain manager might also participate in meetings, trainings, and workshops to share information, learn new skills, and collaborate with other stakeholders. They might also conduct research and benchmarking to keep up with the latest trends and innovations in the supply chain field.

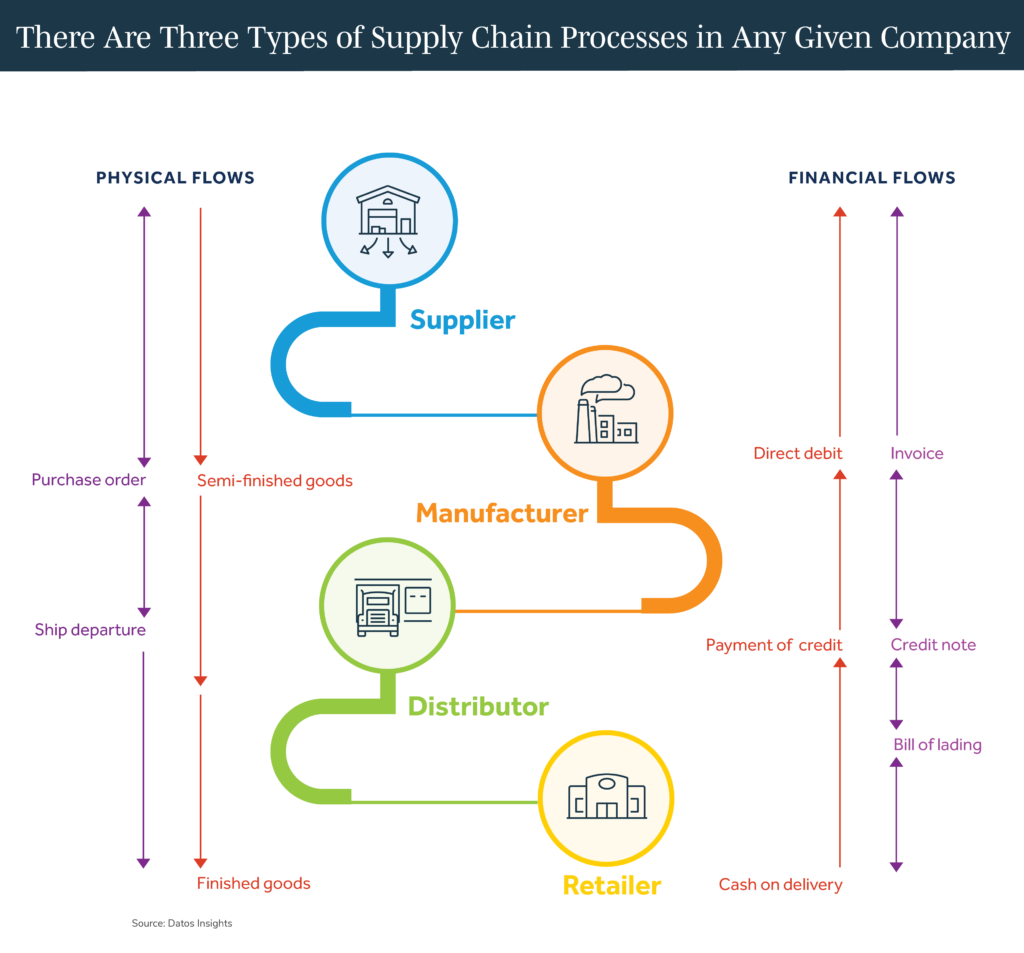

The supply chain processes of any company, large or small, are the steps that transform raw materials into finished products or services. It is important, at this point, to review these processes to understand how they affect the company’s performance, efficiency, and customer satisfaction, as shown in the figure below.

Figure 1: Supply Chain Processes

The physical flows and the financial flows are two types of flows in a supply chain. The physical flows are the movements of raw materials in addition to semi-finished and finished goods from the supplier to the buyer. The financial flows are the payments that go from the buyer to the supplier. They move in opposite directions of each other.

Another crucial aspect of the supply chain is the information flow that connects all the parties involved in the physical movement of goods and services. The information flow includes data and documents that are generated by the physical flow, such as invoices, credit/debit notes receipts, purchase and sales orders, and delivery confirmations.

These information elements often trigger financial transactions, such as payments, collections, or loan applications. These are the components of the financial supply chain (FSC) that enable the smooth functioning of the business operations. In other words, life-cycle banking delivers FSC capabilities triggered by physical supply chain (PSC) events.

Life-cycle banking, however, is not very precise and can mean different things to different people. To illustrate how life-cycle banking works, let’s look at a scenario of a business customer who uses it.

Life-Cycle Banking in Practice

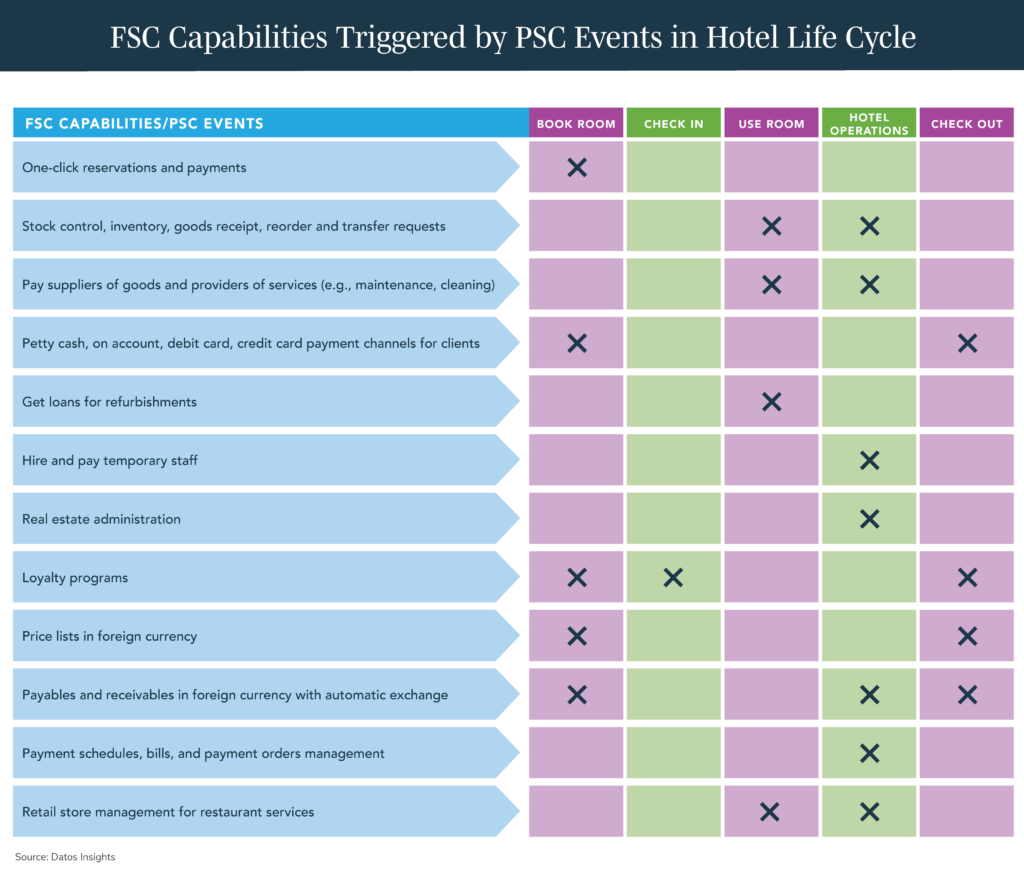

For instance, let’s check the business of running a hotel with a brief set of examples of FSC flows for this specific sector:

- One-click reservations and payments

- Stock control, inventory, goods receipt, reorder and transfer requests

- Pay suppliers of goods and providers of services (e.g., maintenance, cleaning)

- Petty cash, on account, debit card, credit card payment channels for clients

- Get loans for refurbishments

- Hire and pay temporary staff

- Real estate administration

- Loyalty programs

- Price lists in foreign currency

- Payables and receivables in foreign currency with automatic exchange

- Payment schedules, bills, and payment orders management

- Retail store management for restaurant services

Figure 2, below, helps to visualize how the FSC capabilities relate to the PSC events in a hotel business.

Figure 2: FSC Capabilities Triggered by PSC Events Typical of Hotel Life Cycle

The table has one row for each FSC capability and one column for each PSC event. For example, the first row shows that reservation—and consequent payment—are triggered by the events of booking, check-in, stay, and checkout. When the client is checking in, that event will trigger the hotel system to pop up loyalty programs and discount/special price facilities. After a client used a room, the hotel system automates the payment process to the suppliers and service providers who are involved in the room usage, such as maintenance and cleaning staff.

This use case that explains how FSC capabilities are linked to (and triggered by) PSC events can be extrapolated from the hotel industry segment to any other business sector. The system records the data exchanged in each transaction based on the PSC triggers and the FSC capabilities. When goods are shipped, delivered, or returned, they generate data that can be used to optimize financial processes.

Such data can help reduce costs, improve cash flow, and mitigate risks. As seen for the hotel industry, data from PSC events can enable faster invoicing, better inventory management, and more accurate forecasting. This is how FSC capabilities are triggered by PSC events.

And this is the essence of life-cycle banking. Life-cycle banking is a way of providing financial services that are linked to the events and needs of the PSC. It uses Banking-as-a-Service components that can be customized and consumed according to the industry sector. Life-cycle banking aims to optimize the FSC for different stages of production and distribution.

Life-cycle banking is a way of providing banking services that are tailored to the specific needs and goals of a specific sector. It involves following the sector-specific process flows to execute banking capabilities, such as creating, processing, and storing data. By doing so, life-cycle banking maximizes the value of the data exchanged between banks and their enterprise customers.

Have questions about how life-cycle banking works? Contact me here. And stay tuned for part two of this blog series next week, where I will explore use cases of life-cycle banking across the entire supply chain.