The securities and investments industry is characterized by cobbled-together data-hungry specialty technology that passes trades, transactions, and reconciling positions and corporate actions across disparate applications. This model has worked for years, but shorter settlement cycles, increased volume, and a never-ending list of new regulatory reporting requirements have the model creaking at its seams.

Drivers for Change

Data management has been on a long, slow evolutionary path. Now, the pace of evolution is accelerating. Datos Insights sees four key components driving this acceleration:

- Business/data alignment: Shorter settlement cycles require much tighter data alignment across applications and a single data source to power accounting books of record and investment books of record.

- Increased complexity: In the search for alpha, firms are expanding their use of private assets, real assets, and other alternative data sources. Evolving environmental, social, and corporate governance (ESG) regulations are also adding layers to existing security masters.

- Systems consolidation/simplification: The trend toward moving to single front-to-back core systems simplifies the technology stack and, in many cases, provides those incumbent solutions an opportunity to offer managed data services as additional value-added components.

- Technology: Cloud data-sharing technologies such as Snowflake have created new ways to share data across applications, unlocking integration challenges with hybrid deployed businesses and creating a new platform to support data sharing across businesses. Artificial intelligence is being deployed to support everything from the normalization of unstructured data to the reconciliation and data enrichment needs across business applications. These new capabilities and a growing appetite for managed services set the stage for step change and significant growth. However, this remains a market in its infancy.

Against this backdrop, buyers have more choices than ever, but this comes at a cost: Buyers have much more provider noise to sort through. It seems as if every provider, from reconciliations to accounting, is rebranding itself as a “data management” provider, and every provider seems to offer some flavor of managed data services.

Buyers: Spoiled for Choice?

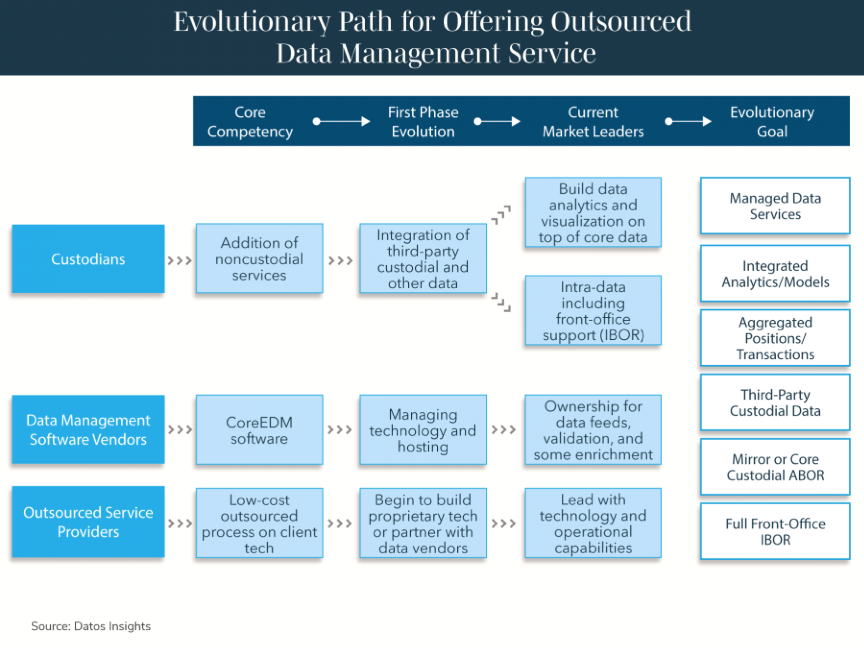

For solution providers, the race is on to add the combination of technology, expertise, and operational scalability to address the market’s needs. As the market shakes itself out, Datos Insights is seeing solutions emerge from four broad categories: custodians, enterprise data management (EDM) software vendors, traditional outsourcing providers, and others, i.e., firms leveraging core processing capabilities.

- Custodians: These providers extend middle-office outsourced services and expertise in managing their clients’ accounting books of record and add data management services.

- EDM software vendors: This group actively builds and partners with third-party outsourced providers to offer managed services on top of their solutions.

- Traditional outsource providers: These providers typically leverage in-house or third-party technology capabilities to create and manage client data.

- Others: Data-heavy applications from trading to accounting systems support the ingestion and reconciliation of data. Datos Insights believes these systems will spin off their own capabilities.

The figure below highlights the evolutionary path of these providers.

Looking at the progression toward managed data services, we’re only seeing the first generation of these solutions in the market in most cases. Most, if not all, remain incomplete solutions. Solution providers are still building asset class capabilities and determining how to manage indices, data contracts, integrations, and hundreds of other complexities. As they do, they will begin to move toward a single data model that masters price, reference, index, ESG, and client-specific data in a way that creates a cloud-enabled and accessible single source of mastered data with full lineage and governance.

The journey will not be smooth, and we will see challenges and failures along the way. But to be clear, this ship has sailed. Firms need to decide if their long-term operating model will include an insourced or outsourced data function, as that long-term strategy impacts 2024 operating and technology architecture.

For more, see Datos Insights’ The Good, the Bad, and the Evolution of Managed Data Services.